Dreaming of a peaceful getaway spot is exciting. But, making it real needs careful money planning. You must know how much you can buy before looking at properties.

A mortgage calculator for assessing the affordability of vacation homes helps a lot. It lets you see if your budget fits the monthly costs. This way, your dream home won’t be a money problem.

A good mortgage affordability calculator guides you through buying a second home. Just put in your income, debts, and savings. You’ll see what you can really afford. Responsible ownership starts with knowing your limits, for your wealth and peace of mind.

Vacation Home Affordability Calculator

Estimate the vacation-home price you may be able to afford based on your income, debts, down payment, current housing costs and the full monthly cost of owning a second home.

Income and existing obligations

Cash available and loan details

Vacation-home ownership costs

Key Takeaways

- Determine your actual budget before searching for a second property.

- Use digital tools to estimate monthly payments and interest rates accurately.

- Understand how existing debt impacts your ability to secure new financing.

- Prioritize long-term financial health over short-term emotional impulses.

- Gain confidence in your purchasing power through precise data analysis.

Understanding the Importance of a Mortgage Calculator

A mortgage calculator is key for any real estate plan. It takes your financial info and makes it easy to see your future. This helps you plan better.

What is a Mortgage Calculator?

This tool looks at your income, debt, and down payment. It shows how much you can borrow each month. It’s like having a virtual financial advisor to guide you.

Using a vacation property calculator gives you a clear view of costs. You’ll see how your money choices affect your second home plans.

Benefits of Using a Mortgage Calculator

The main benefit is seeing different financial scenarios. You can change interest rates and loan terms. This shows how they affect your monthly budget.

Knowledge is power when investing in real estate. A vacation property calculator helps you make smart choices. You’ll know your decisions are based on accurate data.

These tools show how your current debt affects your future goals. This clarity is the first step to making a smart financial choice.

Factors to Consider When Choosing a Vacation Home

When you look for vacation homes, don’t just look at how it looks. The real cost of owning a home is more than the first price you see. There are hidden costs that can affect your investment over time.

Location and Market Trends

The place where your home is located is very important. You should check if the area is growing or if property values are staying the same.

Being close to popular places helps you rent out your home when you’re not there. A good location makes your vacation homes more attractive in a competitive market.

Property Type and Features

Every home has its own special needs. Look at the home’s age, how well it was built, and its layout before you buy.

Also, check how far it is to important places like hospitals and grocery stores. Choosing vacation homes with modern features and good construction can save you money later.

Maintenance and Upkeep Costs

Many people forget about the costs of owning a second home. You need to think about regular upkeep, seasonal work, and big repairs that might happen.

Renovations can become a big problem if you don’t plan for them. By thinking about these costs, you can make sure your vacation homes are a place of peace and happiness for a long time.

How to Use a Mortgage Calculator Effectively

Getting your finances right starts with the right info in a mortgage calculator. By putting in your details right, you turn numbers into a clear plan for your future. This is key for anyone serious about buying a home.

Inputting Your Financial Information

To get the best from this home buying tool, give accurate info on your income and debts. Right numbers mean better guesses on your monthly payments and what you can buy.

Don’t forget your down payment. A big one can change your financial future and get you better loan deals. Being consistent with your data makes sure the results match your real situation.

Understanding Loan Terms and Interest Rates

After setting your base, try different loan terms and rates. This home buying tool shows how small changes can affect your budget. It helps you see your financial future better.

Knowing these details is key for smart choices. Whether it’s a short or long mortgage, a calculator shows the total cost. This insight helps your vacation home stay a good investment, not a financial stress.

Debt-to-Income Ratio Explained

Your financial health is measured by your debt-to-income ratio. This is key when you calculate mortgage for vacation home costs. Lenders check this to see if you can handle monthly payments and other debts.

How to Calculate Your Debt-to-Income Ratio

To find your ratio, add up all your monthly debt payments. This includes your mortgage, student loans, car payments, and credit card minimums. Don’t count living costs like food or utilities in this total.

Then, divide your total monthly debt by your gross monthly income. This is your pay before taxes. Multiply by 100 to get your percentage. This shows lenders how much you can borrow.

Why It Matters for Vacation Home Financing

Lenders use the 28/36 rule to check your risk. This means your housing costs should be no more than 28% of your income. Your total debt should be under 36%.

Keeping your ratio low shows you can handle a second property. If it’s too high, you might need to pay off debts first. Prioritizing debt reduction can get you better rates and easier loan approval.

The Role of Credit Scores in Mortgage Approval

Before you look for a vacation home, know how your credit score matters. Lenders see your credit history as a sign of your financial reliability. This three-digit number is key when you apply for a mortgage.

How Credit Scores Affect Interest Rates

A better credit score means you might get favorable interest rates. Lenders see you as less risky, so they offer better loan terms. These small differences can save you a lot over time.

A lower score might mean higher rates or even a loan denial. Lenders check if you can handle the debt of a second property. Keeping a strong credit score helps keep your monthly payments low.

| Credit Score Range | Interest Rate Impact | Approval Likelihood |

|---|---|---|

| 760 – 850 | Excellent (Lowest) | Very High |

| 700 – 759 | Good (Competitive) | High |

| 620 – 699 | Fair (Higher) | Moderate |

| Below 620 | Poor (Highest) | Low |

Improving Your Credit Score Before Applying

Strengthening your credit before applying can really help. Paying down debt lowers your credit use ratio. This shows lenders you’re good with money.

Check your credit report for errors. Fixing mistakes can improve your score. Consistency is key; make all payments on time before applying.

Comparing Different Mortgage Options

Understanding home financing is key to growing your wealth. Choosing the right mortgage is a big decision. It depends on your financial goals and how long you’ll own the property. Use an affordability mortgage calculator to see how different rates affect your payments.

Fixed-Rate Mortgages vs. Adjustable-Rate Mortgages

A fixed-rate mortgage means your payments stay the same. This protects you from market changes. It helps you budget for your vacation home.

An adjustable-rate mortgage (ARM) starts with a lower rate for a while. It’s good for short-term ownership or if your income will grow. But, be ready for higher payments later.

“The best way to predict your financial future is to create it through informed decision-making and careful planning.”

Government-Backed Loans vs. Conventional Loans

There are conventional loans and government-backed loans. Conventional loans need better credit and a bigger down payment. They’re for buyers with strong finances and want flexibility.

Government-backed loans, like FHA or VA, have easier credit rules and smaller down payments. They’re great for primary homes. But, check if they work for vacation homes too. Knowing this helps you pick a loan that saves you money and keeps your cash flow good.

Estimating Down Payments and Closing Costs

Getting your dream vacation home is more than just the price. You need to think about the money you need upfront. Knowing these costs helps keep your budget safe during the buying process. Proper preparation makes everything go smoothly.

Typical Down Payment Requirements

A big down payment can lower your loan amount. Many aim for 20% down, but less is okay too. Private mortgage insurance (PMI) is needed for less than 20% down.

Less down means less cash upfront but more PMI. This means higher monthly payments. Think about your money now and your future goals. Careful calculation helps choose the right down payment for you.

Additional Closing Costs to Consider

There are costs besides the down payment when buying a home. These include property taxes, lender fees, and title insurance. Unexpected costs can add up fast. It’s smart to save extra money early on.

Closing costs usually are 2% to 5% of the loan amount. Ask your lender for a Loan Estimate to see these costs. Being proactive about these fees avoids last-minute money worries when closing your vacation home.

Assessing Long-Term Financial Responsibilities

Your vacation home needs ongoing money care. The mortgage is a big part, but not all. Planning for recurring expenses keeps your investment fun, not a money drain.

Property Taxes and Insurance Considerations

Property taxes change based on where you live and your home’s value. They are required and can go up or down. Look into your area’s tax history to avoid unexpected financial surprises.

Don’t forget about homeowners insurance. It’s key to protect your home from disasters, theft, or lawsuits. Securing a comprehensive policy gives you peace of mind, especially when your home is empty.

Potential Rental Income from Vacation Properties

Many owners rent out their homes to cover costs. This can make your home a sustainable long-term financial asset. Rental income can help pay for taxes, insurance, and upkeep.

But, being a landlord has its own challenges. You’ll need to handle bookings, cleaning, and guest needs. If you use a property manager, add their fees to your overall budget calculations to keep things profitable.

Common Mistakes to Avoid in Vacation Home Buying

Buying vacation homes is exciting, but it’s important to avoid money mistakes. Many people only look at the price and forget about the long-term effects. To make sure your investment is good, you need a solid plan.

Overextending Your Budget

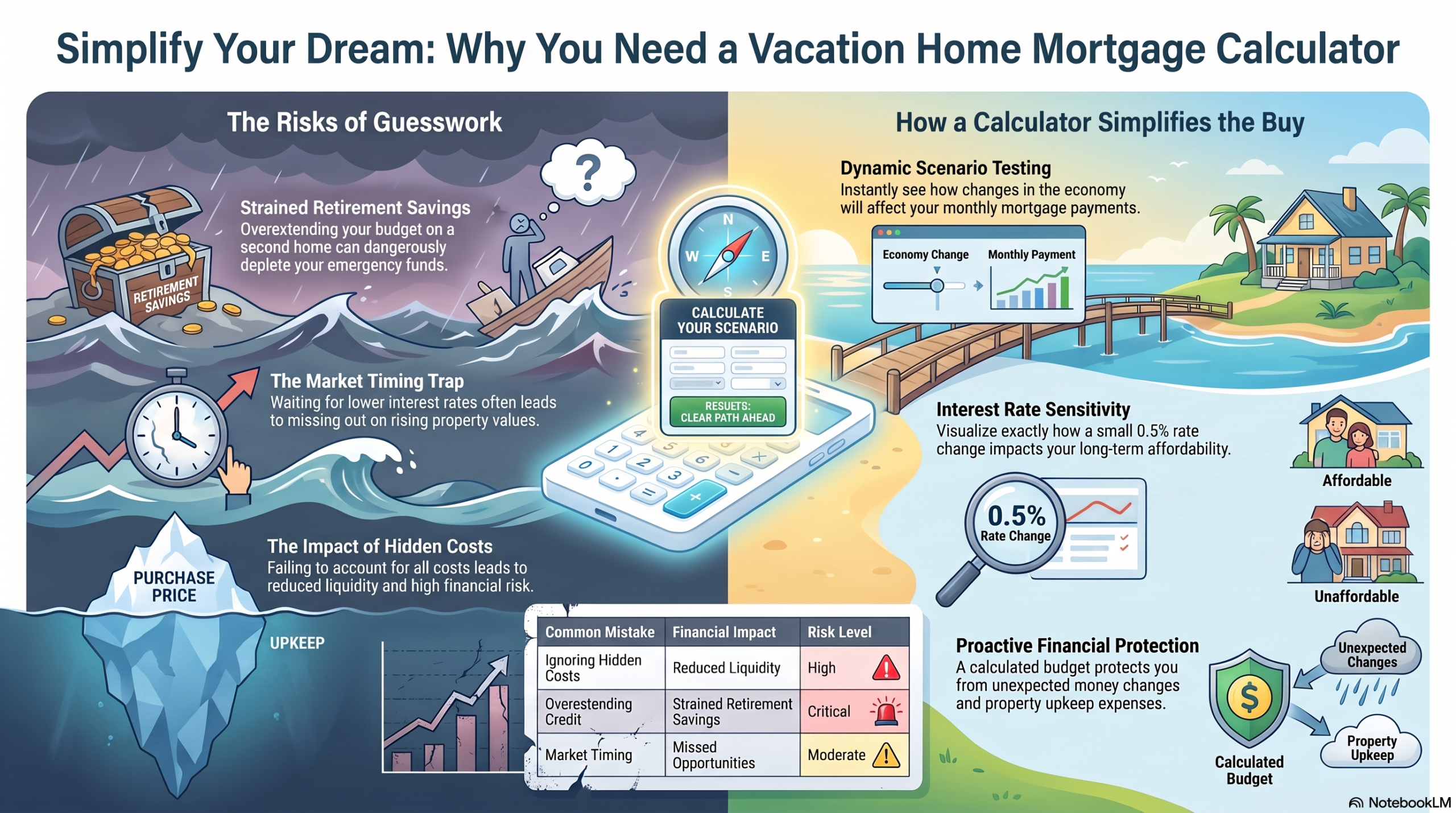

One big mistake is not having a real vacation home budget that includes all costs. You might want to spend more to get your dream home. But, this can hurt your savings for retirement or emergencies. Financial stability is more important than a second home.

Spending too much can leave you with no money for repairs or upkeep. It’s smart to check expert tips to keep your future safe. A good vacation home budget protects you from unexpected money changes.

Neglecting Future Market Conditions

Some people wait for the best interest rates to buy vacation homes. But, home prices in tourist spots might go up. It’s better to think about what you can afford now, not wait for the perfect rate.

The market can change quickly and unpredictably. Instead of guessing what will happen, buy a home that you can afford now. This way, you avoid stress and keep your investment safe.

| Common Mistake | Financial Impact | Risk Level |

|---|---|---|

| Ignoring Hidden Costs | Reduced Liquidity | High |

| Overextending Credit | Strained Retirement Savings | Critical |

| Market Timing | Missed Opportunities | Moderate |

| Underestimating Upkeep | Declining Property Value | Moderate |

Using Your Mortgage Calculator for Different Scenarios

Testing different financial scenarios is key to a smart vacation home buy. A good mortgage calculator lets you see how changes in the economy affect your payments. This helps you check if your budget can handle big financial steps.

Exploring Various Interest Rates

Interest rates can change a lot, even a little bit. Use your second home calculator to see how a 0.5% rate change affects your budget. This shows if you can still afford your dream home, even with market ups and downs.

Seeing these changes helps you know your financial limits. If a small rate increase makes it too expensive, think about a bigger down payment. Or maybe look for a home that costs less. For more on using your home’s equity, check out a home equity loan calculator.

Adjusting for Extra Payments

Pay off your vacation home loan faster to save money. A second home calculator shows the benefits of extra payments. Even a little extra each month can make a big difference over time.

Here are some benefits of paying more:

- Reduced Interest Costs: Adding $100 to your monthly payment can save you thousands in interest over years.

- Shorter Loan Term: Extra payments can cut years off your mortgage, letting you own your home sooner.

- Increased Equity: Paying down faster builds your equity faster, giving you more financial freedom later.

Try out different payment plans with your mortgage calculator. This turns numbers into a plan for financial freedom.

Making Informed Decisions with Your Results

Looking at your money helps you see how much you can afford. You’ll know if a vacation home is right for you and your budget.

Understanding Your Affordability Limit

Getting prequalified is a big step. It tells you how much you can borrow without hurting your credit score. This helps you find homes that fit your budget and future plans.

Planning Beyond the Purchase

Having a vacation home means you’ll need to take care of it. Think about maintenance, property management, taxes, insurance, and repairs. Use tools like Zillow or Redfin to keep up with the market. But, your budget is the most important thing for long-term success. Plan well to enjoy your home for years.