Key Takeaways

- Gain financial clarity before touring properties in the North Star State.

- Use digital tools to assess your budget and debt profile accurately.

- Determine a realistic price range to streamline your home search.

- Reduce stress by understanding your monthly payment obligations early.

- Set a strong foundation for a successful and informed purchase.

Understanding How a Mortgage Calculator Works

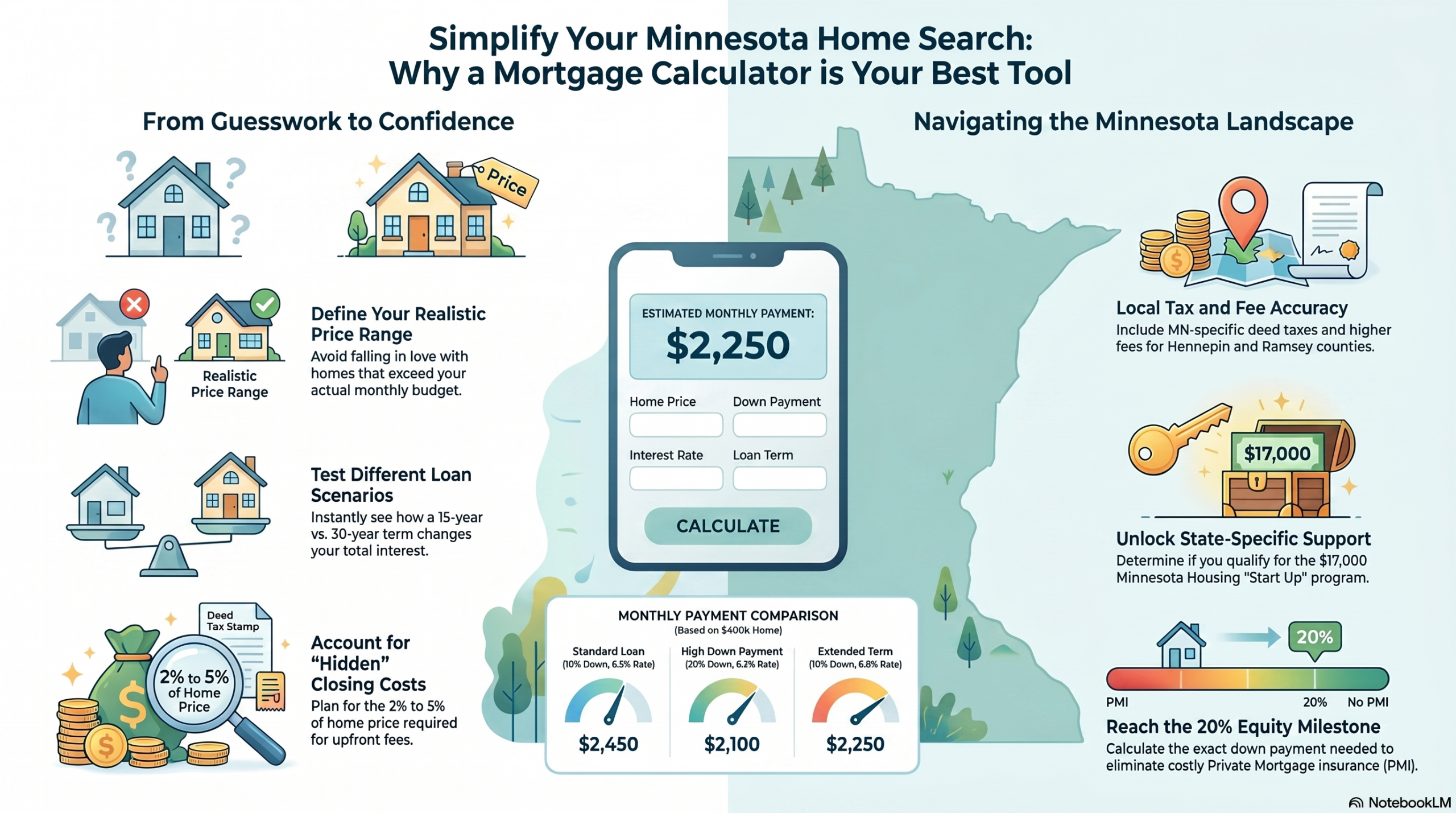

An online mortgage calculator Minnesota folks use makes complex math simple. Just enter a few numbers, and you see your future financial picture. It connects numbers to your home buying budget.

Key Components of a Mortgage Calculator

To get a good estimate, know the main parts. The principal is the loan amount for your home. The interest rate is the cost of that loan, shown as an annual percent.

The loan term is how long you’ll pay back the loan. Most loans last fifteen or thirty years. These three parts are the base of every calculation.

How Calculations Are Made

These tools use a special formula to figure out your monthly payment. The formula is M = P[r(1+r)^n]/[(1+r)^n-1]. Here, M is your monthly payment, and P is the loan amount.

The variable r is your monthly interest rate, and n is the total payments over the loan’s life. An online mortgage calculator Minnesota users trust gives a precise monthly payment.

The Importance of Accurate Inputs

Your results depend on the data you give. Wrong numbers mean wrong results. Always check your interest rate and down payment before budgeting.

Using an online mortgage calculator Minnesota tool with accurate info helps you plan better. Realistic inputs mean no surprises later. Being precise now saves you stress later.

Benefits of Using a Minnesota Mortgage Calculator

Using a digital tool can change your home-buying journey. It turns it from a stressful guess game into a clear plan. The best mortgage calculator MN offers helps you make smart choices in a tough market.

Simplifying Complex Calculations

Mortgage math has many tricky parts like property taxes and interest rates. A good Minnesota mortgage affordability calculator makes these easy to understand. It turns complex numbers into simple monthly costs. This saves time and avoids mistakes.

Budgeting for Your New Home

Having a solid budget is key to buying a home. These calculators let you see how much you can afford. By knowing your limits, you won’t fall in love with a home that’s too expensive.

Evaluating Different Loan Scenarios

These tools help you compare different loan options. You can see how a bigger down payment changes your costs. The table below shows how different choices might affect your monthly payments.

| Scenario | Down Payment | Interest Rate | Monthly Payment |

|---|---|---|---|

| Standard Loan | 10% | 6.5% | $2,450 |

| High Down Payment | 20% | 6.2% | $2,100 |

| Extended Term | 10% | 6.8% | $2,250 |

Types of Mortgages Available in Minnesota

Choosing the right home loan is key to owning a home in Minnesota. Lenders offer many options to fit your financial needs. A Minnesota home loan calculator helps see how each loan affects your monthly costs.

Fixed-Rate Mortgages Explained

A fixed-rate mortgage is great for those who like predictability. Your interest rate stays the same for 15 or 30 years.

With fixed payments, you can plan your finances well. This keeps your costs steady, even when the market changes.

Adjustable-Rate Mortgages Overview

Adjustable-rate mortgages, or ARMs, start with a lower rate. This period is usually three, five, or seven years, making early payments cheaper.

But, after this period, your rate can change with the market. Think carefully about this choice, as your payments might go up a lot.

Government-Backed Loans

Government-backed loans help first-time buyers or those with less savings. They offer flexible credit and lower down payments.

Some common ones are:

- FHA Loans: Good for buyers with lower credit scores or smaller down payments.

- VA Loans: For veterans and active-duty military, often no down payment needed.

- USDA Loans: For buyers in rural areas, with competitive terms.

Conventional loans are also popular, needing only 3 percent down for some. No matter the loan, a Minnesota home loan calculator helps you see the total cost before you sign.

Factors Affecting Your Mortgage Payments

Many things affect how much you pay each month for your home. The loan amount is just the start. Other things can change your monthly payments a lot. Knowing these can help you avoid surprises when you own a home.

Interest Rates and Their Impact

Your interest rate is very important for your costs over time. A small change in mortgage rates in Minnesota can mean a big difference in money. A lower rate means you pay less each month and less interest to the lender.

“The best time to plant a tree was twenty years ago. The second best time is now.”

Interest rates change with the market. Getting a good rate means a more stable financial future. Keep an eye on rates to see if they fit your budget.

Loan Terms Explained

The loan term is how long you take to pay off your mortgage. Most people choose between 15 and 30 years. A shorter term means higher payments but less interest.

A longer term means smaller payments but more interest over time. Picking the right term is about balancing what you can pay now and what you want for the future.

Property Taxes and Insurance Costs

Lenders often ask you to save for property taxes and insurance. These are added to your monthly payment. In Minnesota, property taxes are usually 0.5% to 2.5% of the home’s value each year.

These costs can change based on where you live and your home’s value. Planning for these costs helps you stay ready for any changes. This way, you know exactly what you’ll pay each month, including mortgage rates in Minnesota and elsewhere.

How to Estimate Your Monthly Mortgage Payment

You can easily calculate mortgage in Minnesota by breaking down your total payment into manageable parts. Understanding these figures provides the transparency needed to make confident financial decisions. By demystifying the math, you gain control over your home-buying journey.

Principal and Interest Calculations

The foundation of your monthly bill consists of principal and interest. The principal is the portion of your payment that goes toward reducing your loan balance. The interest is the cost you pay to the lender for borrowing the money.

These two components follow an amortization schedule. Early in your loan term, a larger portion of your payment covers interest. Over time, the balance shifts, and more of your money goes toward paying down the principal.

Incorporating Taxes and Insurance

A complete monthly payment often includes more than just the loan repayment. Most lenders require you to pay property taxes and homeowners insurance through an escrow account. These costs are bundled into your single monthly statement to ensure they are paid on time.

Failing to account for these extra costs can lead to budget surprises. Always include estimates for local tax rates and insurance premiums when you assess your affordability. This ensures your monthly budget remains realistic and sustainable.

Example Scenarios for Better Understanding

To effectively calculate mortgage in Minnesota, it helps to see how these numbers interact. The following table illustrates a hypothetical scenario for a $300,000 home purchase with a 20% down payment.

| Expense Category | Estimated Monthly Cost |

|---|---|

| Principal & Interest | $1,432 |

| Property Taxes | $300 |

| Homeowners Insurance | $100 |

| Total Monthly Payment | $1,832 |

This breakdown shows how individual costs aggregate into your final bill. Always remember that these figures are estimates. Your actual costs may vary based on your specific interest rate, location, and insurance provider.

The Role of Down Payments in Mortgage Calculations

Your down payment is key to your home financing plan. It affects your loan terms and interest over time. When you calculate mortgage in Minnesota, you’ll see how it boosts your financial health.

Minimum Down Payment Requirements

Many think they need a lot to buy a home. But, many loan programs have flexible down payments. Conventional loans might need only 3% down, and FHA loans 3.5%.

Remember, these are just starting points. Lenders look at your debt and income too. Always check your specific needs before planning your budget.

Effect on Monthly Payments

How much you put down affects your monthly payments. If it’s less than 20%, you might need Private Mortgage Insurance (PMI). This insurance helps the lender but increases your monthly costs.

“Equity is the silent partner in your home ownership journey; the more you invest today, the more you secure for your future.”

With 20% down, you avoid PMI. This can save you a lot each month. It makes calculating mortgage in Minnesota easier and clearer.

| Down Payment % | PMI Requirement | Loan-to-Value Ratio |

|---|---|---|

| 3% – 5% | Required | 95% – 97% |

| 10% – 15% | Required | 85% – 90% |

| 20% or more | Not Required | 80% or less |

Strategies for Saving for a Down Payment

Building savings needs discipline and a plan. Start by setting up automatic transfers to a savings account for your home. This keeps your money safe and growing.

Try cutting back on things you don’t need. Even small savings increases can help fast. When you calculate mortgage in Minnesota, you’ll see the benefits of your hard work.

Importance of Credit Score in Mortgage Calculations

Your credit score is like a report card for lenders. It shows how good you are with money. When you use a Minnesota mortgage payment calculator, your score helps decide your interest rate.

What is a Good Credit Score?

Lenders like scores of 740 or higher. These scores get you the best rates. Scores from 670 to 739 are okay, but below 580 is tough.

Maintaining a high score shows you’re good with money. It means you handle debt well.

How Credit Affects Your Interest Rate

Your score affects your mortgage rate. A better score means a lower rate. This lowers your monthly payments over time.

Try different rates in a Minnesota mortgage payment calculator. Even a small change can save a lot of money.

| Credit Score Range | Borrower Rating | Interest Rate Impact |

|---|---|---|

| 740 – 850 | Excellent | Lowest possible rates |

| 670 – 739 | Good | Competitive market rates |

| 580 – 669 | Fair | Higher interest rates |

| 300 – 579 | Poor | Difficult to qualify |

Steps to Improve Your Credit Score

To improve your score, pay bills on time. This is the best way to raise your score. Also, keep your credit card balances low.

Check your credit reports for mistakes. If you find errors, tell the credit bureaus right away. This keeps your score accurate. By doing these things, you’re ready for better financing when you use a Minnesota mortgage payment calculator.

Utilizing the Minnesota Mortgage Calculator Effectively

Home loans can be easier to understand with the right tools. A Minnesota Mortgage Calculator helps turn complex numbers into a clear plan for your future.

Step-by-Step Guide to Using the Calculator

First, go to a trusted Minnesota mortgage payment calculator. Enter the home price and down payment you’re thinking about.

Then, choose your loan term, like 15 or 30 years. Also, add the current interest rate. Being accurate here is key because small changes can affect your monthly payments a lot.

Understanding the Results Generated

After you enter your info, the calculator shows your estimated monthly payment. This includes principal, interest, property taxes, and insurance.

“The goal of financial planning is not just to see the numbers, but to understand the story they tell about your future stability.”

Looking at these results helps you see how much goes to interest versus paying off the loan. This amortization schedule is a great tool for planning ahead.

Adjusting Inputs for Different Scenarios

A Minnesota Mortgage Calculator lets you try different scenarios. You can change your down payment to see how it affects your monthly payments. Or, you can see how a shorter loan term changes your total interest paid.

By trying these changes, you feel more sure about your budget. Using a Minnesota mortgage payment calculator helps you make informed decisions that fit your financial goals.

Common Mistakes to Avoid with Mortgage Calculators

Getting a mortgage needs careful planning. But, many buyers make mistakes with online tools. The best mortgage calculator MN users have is helpful, but it’s only as good as the info you give it. If you put in wrong data, your plans won’t be right.

Inputting Incorrect Data

Most people make the mistake of using guesses instead of real numbers. Make sure your interest rate, loan term, and down payment are correct. A tiny mistake in interest rate can change your monthly payments a lot.

Always check your local property taxes and homeowners insurance before you start. Using national averages instead of Minnesota data can give you misleading results. When using the best mortgage calculator MN, look up your county’s specific needs.

Misunderstanding the Results

Many first-time buyers think calculator results are final loan offers. But, these tools give estimates only. They don’t consider your credit, debt, or lender rules.

See these results as a starting point, not a final plan. Always talk to a loan officer for a real pre-approval. Relying only on online tools can lead to disappointment later.

Neglecting Additional Costs

Many forget to add closing costs to their budget. These costs are usually two percent to five percent of the home’s price. They can add thousands to what you need upfront.

Don’t forget to plan for appraisal fees, title insurance, and origination charges. Not including these can make your home seem cheaper than it is. Here’s how missing these costs can affect your budget.

| Common Mistake | Potential Impact | Corrective Action |

|---|---|---|

| Ignoring Closing Costs | Budget shortfall | Add 3-5% to cash reserves |

| Using Generic Tax Rates | Underestimated payments | Check local county tax records |

| Assuming Fixed Rates | Payment volatility | Test multiple interest scenarios |

| Overlooking Insurance | Inaccurate monthly budget | Get quotes from local providers |

Comparing Multiple Mortgage Offers

Looking at many mortgage options is smart for your money. You can see how each loan affects your monthly costs and total interest over time.

How to Use the Calculator for Comparisons

Put each loan’s details into your calculator one by one. Note the monthly payment and total interest for each. This helps you choose the best option for you.

When checking mortgage rates in Minnesota, remember a lower rate isn’t always the best. Look at all costs to make sure you’re getting a good deal.

Factors to Consider Beyond Interest Rates

Interest rates are important, but not the only thing. Also, think about closing costs, fees, and the loan term.

“The bitterness of poor quality remains long after the sweetness of low price is forgotten.”

Comparing a 15-year and 30-year mortgage shows big differences. The 15-year option has higher monthly payments but saves money in the long run.

Identifying the Best Overall Deal

The best deal balances your now and future money needs. Use your calculator to see how different down payments or loan types affect your costs.

These methods are also good for using a refinance calculator Minnesota tool. By carefully comparing, your home purchase stays a good investment for years.

Resources for Home Buyers in Minnesota

Buying a home in Minnesota is more than a dream. It needs the right tools and support. A Minnesota home loan calculator helps with your budget. But, talking to local experts is key to understanding the housing market.

Local Housing Market Insights

Knowing the local market trends is crucial. It helps you make a strong offer. Look at local prices and how many homes are for sale.

Local real estate groups share important data. This helps you set realistic goals. It makes sure your money plans match the Minnesota housing market.

Financial Counselling Services

Getting ready for a mortgage needs expert help. Financial advisors offer invaluable support. They check your credit, help with debt, and plan for savings.

- Reviewing your debt-to-income ratio.

- Creating a personalized budget for home maintenance.

- Understanding the long-term impact of interest rates.

State-Specific Lending Programs

Minnesota has great help for homebuyers. The Minnesota Housing “Start Up” program is a big help.

This program gives up to $17,000 for down payments and closing costs. It makes buying a home easier. Whether it’s your first home or a refinance, these programs are here to help.

Final Thoughts on Using a Minnesota Mortgage Calculator

Getting ready to buy a home needs careful planning. A Minnesota mortgage calculator helps you see your finances clearly. It’s a key tool for understanding the housing market.

Making Informed Decisions

Numbers help you compare loans and rates. You learn how your down payment changes your monthly costs. This helps you find a home that fits your financial plans.

The Importance of Professional Guidance

Online tools give estimates, but a real expert is needed. A licensed lender can guide you through special programs. They help you understand your credit and local taxes.

Planning for Your Home Purchase Journey

Buying a home is a big step. Using a mortgage calculator helps you plan for the future. Stay on track with your budget and talk to experts to make your dream come true.