Beyond the Estimate: Calculating Your HECM Reverse Mortgage

For many retirees, the “Retirement Equity Puzzle” represents a structural flaw in traditional retirement planning. We often obsess over portfolio volatility and liquid assets while ignoring our largest store of stagnant capital: home equity. A Home Equity Conversion Mortgage (HECM) calculator is far more than a simple estimator; it is a strategic financial crystal ball that can reveal how to activate your home’s value for multi-decade security.

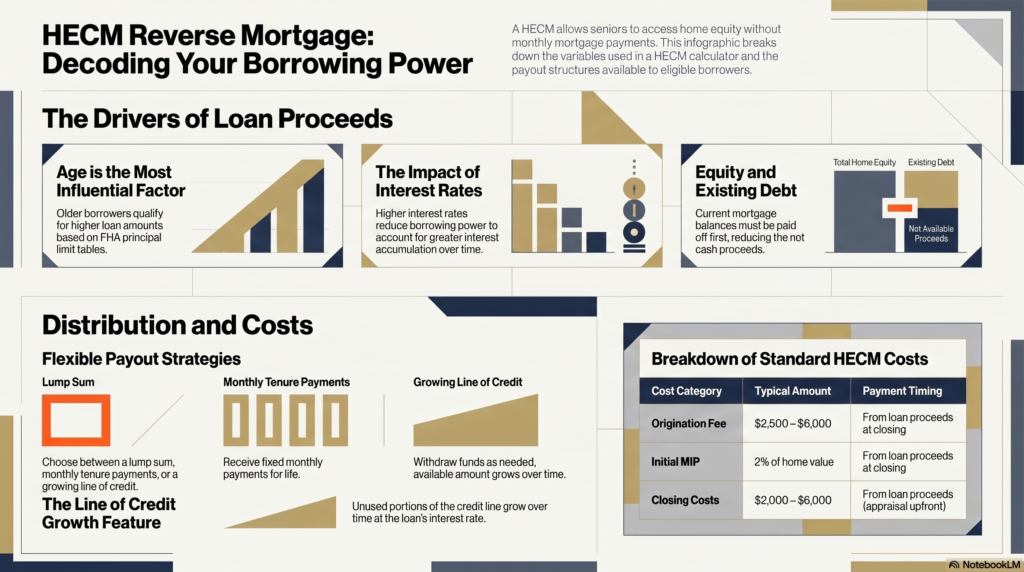

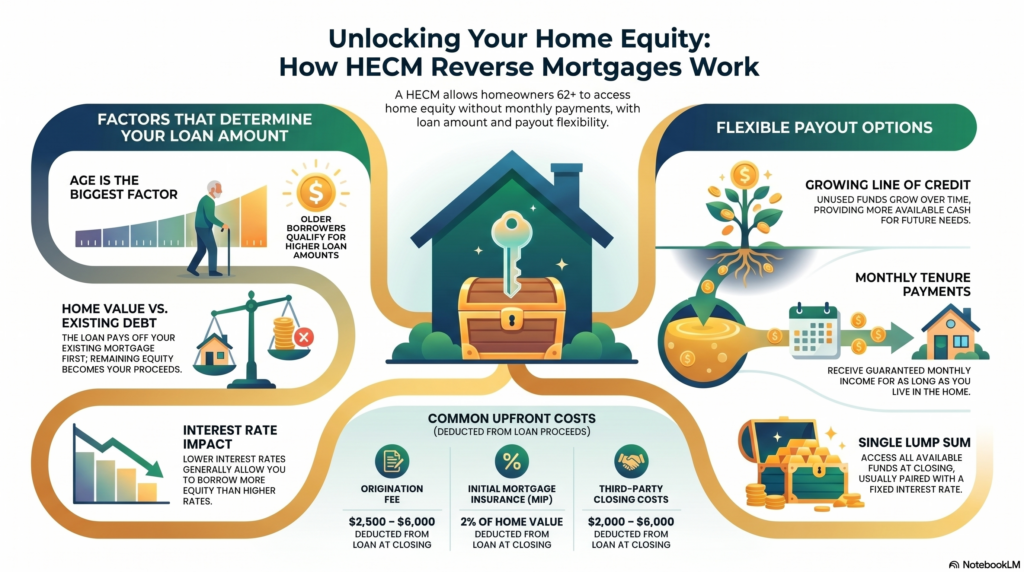

1. Your Age is More Than a Number—It’s a Multiplier

In the world of HECM loans, age serves as a primary driver of borrowing power. Unlike traditional lending, where a longer life expectancy might be viewed as a risk, the HECM system uses an actuarial advantage to reward older participants. It is important to remember that for couples, this “multiplier” is anchored to the age of the youngest spouse on the title.

“The relationship between age and loan amount follows FHA’s principal limit factor tables. These tables show that lending percentages increase as borrowers age. A 62-year-old might access 50% of their home value, while a 75-year-old could potentially access 60% or more.”

This structure creates a unique financial environment in which time is an ally of your borrowing power, not just a liability. While younger seniors (62–69) may benefit from more years of potential credit line growth, older borrowers gain immediate access to a higher Principal Limit Factor, making the HECM a product that rewards those who wait.

Share this post

Subscribe to our newsletter

Keep up with the latest blog posts by staying updated. No spamming: we promise.