For many prospective buyers, house hunting begins with excitement and ends in a fog of mathematical anxiety. The purchase price of a home is often treated as the final word on affordability, yet the reality of home financing often feels like a “black box” of hidden variables. In this environment, a mortgage calculator is far more than a simple digital tool; it serves as a financial crystal ball. By distilling complex formulas into clear projections, it allows you to look past the sticker price and understand the long-term implications of your debt. To navigate the market successfully, you must understand the mechanics behind the numbers.

2. Location is a Line Item: Why Zip Codes Change Your Monthly Budget

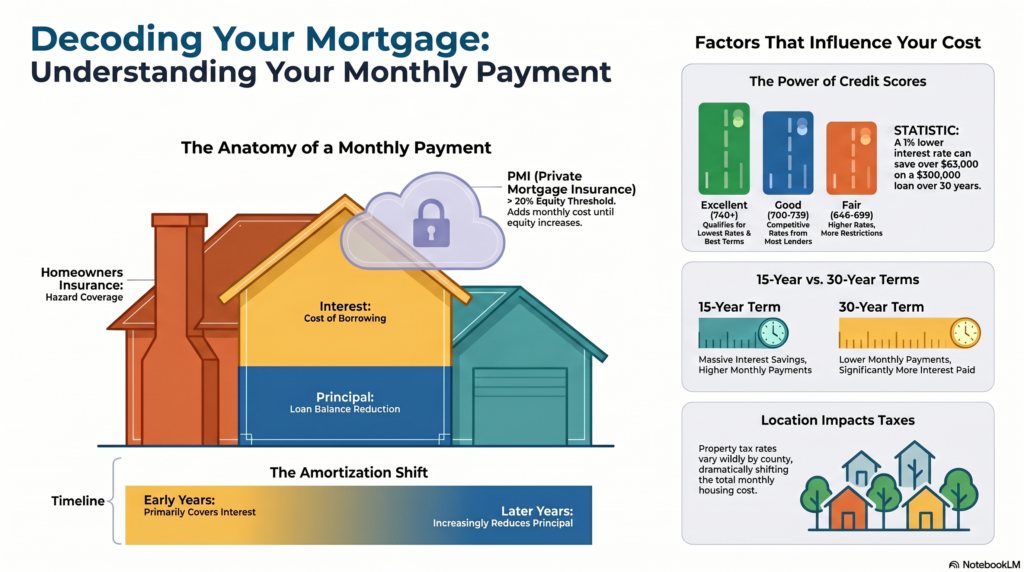

Affordability is often dictated by factors unrelated to the house’s architecture. Property taxes and homeowners’ insurance are location-dependent factors that can significantly affect your monthly budget. Taxes fund local infrastructure like schools and roads, and these rates vary dramatically by geography, typically ranging from 0.5% to 2.5% of the home’s value annually.

Consider the strategic impact of geography:

A $300,000 home in Texas might incur $6,000 in annual property taxes, whereas a home of the same price in Hawaii might incur only $900. That 5,100 annual gap creates a 425 difference in your monthly obligation. When you add varying insurance premiums—which spike in areas prone to natural disasters—your “dream home” in one zip code could be a financial nightmare in another.

Warning: Payment Shock.

Many buyers focus exclusively on principal and interest, only to face “payment shock” when they see the final total. A comprehensive budget must include all escrow items—taxes, insurance, and potentially Homeowners Association (HOA) fees—to reflect the true cost of ownership.