Understanding the HECM Reverse Mortgage Calculator: Your Complete Guide

Making financial decisions during retirement requires careful planning and accurate information. A HECM reverse mortgage calculator serves as an essential tool for seniors exploring ways to access their home equity without monthly mortgage payments. This powerful resource helps homeowners aged 62 and older estimate how much money they might receive through a Home Equity Conversion Mortgage.

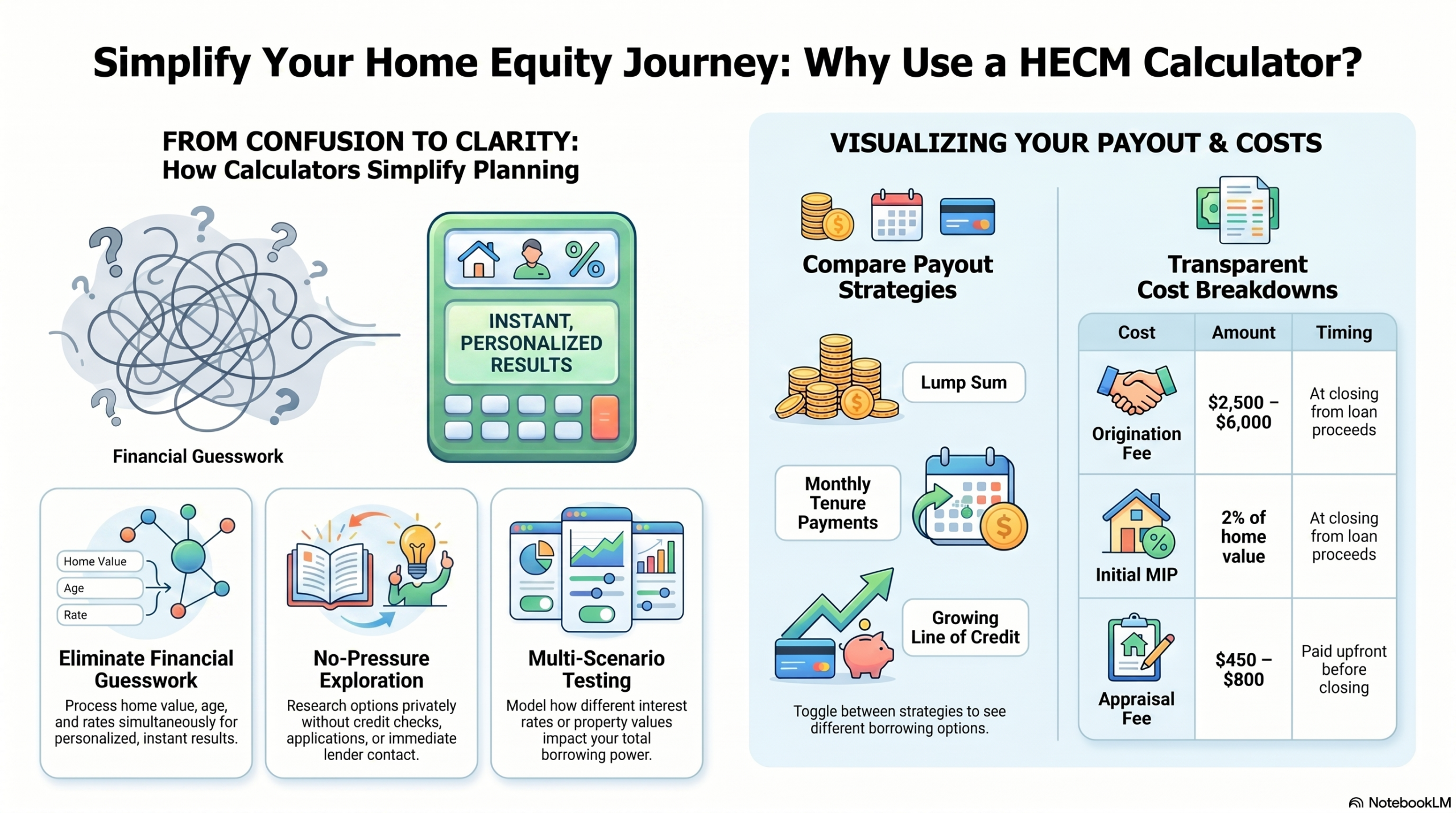

The calculator takes the guesswork out of reverse mortgage planning. It processes multiple factors simultaneously to provide personalized estimates based on your unique situation. Understanding how this tool works empowers you to make informed decisions about your retirement finances.

This comprehensive guide walks you through everything you need to know about HECM calculators. You’ll discover what information these tools analyze, how they generate estimates, and what the results mean for your financial future.

Calculate Your Potential Reverse Mortgage Amount

Discover how much you could access from your home equity with a free HECM calculator. Get instant estimates based on your age, home value, and current interest rates.

What Is a HECM Reverse Mortgage Calculator?

A HECM reverse mortgage calculator is a specialized financial tool designed to estimate the loan proceeds available through a Home Equity Conversion Mortgage. This calculator processes specific data about your home, age, and current market conditions to generate personalized projections. Unlike standard mortgage calculators that focus on payments, this tool shows how much money you can receive.

The calculator represents the most accessible way to understand your reverse mortgage options before speaking with a lender. It functions as a preliminary assessment tool that requires no commitment or credit check. Most online versions take just minutes to complete and provide immediate results.

Core Components of HECM Calculators

Every HECM calculator includes several fundamental input fields that drive the calculation process. These components work together to produce accurate estimates of your potential loan amount. The calculator analyzes each data point according to FHA guidelines and current lending standards.

- Home value input field for current property worth

- Age verification for youngest borrower on title

- Interest rate field using current market rates

- Remaining mortgage balance entry if applicable

- Property type selection for valuation accuracy

How Calculator Results Are Generated

The calculator processes your information through established formulas based on FHA guidelines. It applies principal limit factors that increase with borrower age and decrease with higher interest rates. The tool accounts for mandatory obligations like existing mortgage payoff and closing costs before showing net proceeds.

Results typically appear in multiple formats to help you understand your options. You’ll see total available equity, net loan proceeds after fees, and often different payout options. Some advanced calculators break down costs and show month-by-month projections for line of credit growth.

Key Factors HECM Calculators Consider

HECM calculators evaluate multiple variables to determine your potential loan amount. Each factor plays a significant role in the final calculation, and understanding these elements helps you interpret your results accurately. The interaction between these factors creates your unique borrowing scenario.

Home Value and Property Equity

Your home value serves as the foundation for all reverse mortgage calculations. The calculator uses either your estimated value or a recent appraisal figure to determine the maximum loan limit. FHA sets lending limits that cap the home value used in calculations, regardless of actual property worth.

Current equity in your home directly impacts the net proceeds available to you. The calculator subtracts any existing mortgage balance from the total loan amount to determine what you’ll actually receive. Properties with substantial equity naturally generate larger reverse mortgage proceeds.

Borrower Age and Life Expectancy

Age represents the most influential factor in HECM calculations after home value. Older borrowers qualify for higher loan amounts because actuarial tables predict shorter loan terms. The calculator uses the age of the youngest borrower when multiple people own the property.

The relationship between age and loan amount follows FHA’s principal limit factor tables. These tables increase lending percentages as borrowers age. A 62-year-old might access 50% of their home value, while a 75-year-old could potentially access 60% or more.

Younger Borrowers (62-69)

- Lower initial principal limits

- More years of potential line of credit growth

- Extended time to access increasing credit line

- Conservative lending percentages applied

Older Borrowers (70+)

- Higher initial principal limits

- Greater immediate access to home equity

- Reduced concern about long-term loan costs

- Maximum lending percentages available

Interest Rates and Their Impact

Interest rates significantly affect your reverse mortgage calculation results. Higher interest rates reduce the amount you can borrow because lenders must account for greater accumulation over time. The calculator applies current expected rates, which include both an index and a margin.

Most HECM calculators use adjustable interest rates in their projections. These rates consist of a base index plus a lender margin typically ranging from 2% to 3%. Fixed-rate options exist but generally offer lower initial proceeds because they carry higher initial rates.

Existing Mortgage Balance

Any outstanding mortgage debt must be paid off with reverse mortgage proceeds before you receive funds. The calculator automatically subtracts this balance from your total loan amount. This mandatory payoff eliminates your monthly mortgage payments going forward.

Properties with small remaining balances maximize net proceeds to the borrower. If your existing mortgage consumes a large portion of available equity, you may see limited cash proceeds. The calculator shows both gross loan amount and net proceeds after payoff obligations.

Using a HECM calculator requires gathering specific information about your home and financial situation. The process takes just a few minutes once you have the necessary details ready. Accurate inputs produce reliable estimates that help you understand your borrowing potential.

Gathering Required Information

Before starting your calculation, collect documentation and details about your property and mortgage. Having this information ready ensures accurate results and saves time. You’ll need current figures rather than outdated estimates for the most reliable projections.

- Recent property tax assessment or appraisal value

- Current outstanding mortgage balance statement

- Birth dates for all borrowers on title

- Property type and location information

- Knowledge of any existing liens on property

Step-by-Step Calculation Process

The calculation process follows a straightforward sequence that builds your complete financial picture. Start by entering basic property information, then add personal details, and finally review comprehensive results. Most calculators guide you through each step with clear instructions and helpful tooltips.

Initial Property Details

- Enter estimated home value

- Select property type

- Provide property location

- Confirm primary residence status

Borrower Information

- Input age of youngest borrower

- Specify number of borrowers

- Confirm age eligibility

- Verify ownership status

Financial Obligations

- Enter existing mortgage balance

- Note any other liens

- Include property tax amounts

- Review total obligations

Interpreting Your Results

Calculator results provide multiple data points that paint a complete picture of your reverse mortgage scenario. The primary number shows your total principal limit based on FHA calculations. This represents the maximum amount the lender can provide under current guidelines.

Net proceeds appear after subtracting mandatory obligations and closing costs. This figure represents actual money you could receive or use for your purposes. Pay attention to how different payout options affect these numbers, as lump sum and line of credit choices may show different available amounts.

Many calculators display a breakdown of costs and fees associated with the loan. These typically include origination fees, mortgage insurance premiums, and other closing costs. Understanding these expenses helps you evaluate the true cost of accessing your equity.

Types of Reverse Mortgage Payouts

HECM reverse mortgages offer flexible payment options that adapt to different financial needs and goals. The calculator shows how your total loan amount translates into each payout structure. Choosing the right distribution method depends on your immediate needs and long-term financial plans.

Lump Sum Payment Option

A lump sum payment provides all available funds at closing in one single distribution. This option uses a fixed interest rate rather than an adjustable rate. The calculator shows the exact amount you would receive immediately, though this figure is typically lower than adjustable-rate options.

This payout structure works well for specific large expenses like home renovations or debt consolidation. Once you receive the lump sum, no additional funds remain available to borrow. The entire loan balance begins accruing interest immediately at the fixed rate.

Monthly Payment Plans

Monthly payments from a reverse mortgage function like an annuity from your home equity. You can choose term payments for a specific number of years or tenure payments that continue for life. The calculator divides your available principal limit into equal monthly installments based on your chosen timeframe.

Term payments provide larger monthly amounts over a shorter period. Tenure payments offer smaller amounts but guarantee income for as long as you live in the home. These structured payments help with budgeting and provide predictable monthly income to supplement other retirement funds.

Line of Credit Advantages

The line of credit option provides maximum flexibility and unique growth benefits. You access funds only when needed, and interest accrues only on money actually withdrawn. Unused portions of your credit line grow over time at the same rate as your loan interest rate.

This growth feature distinguishes reverse mortgage credit lines from traditional home equity lines. Your available credit increases automatically without requiring additional applications or approvals. The calculator can project how your credit line expands over five, ten, or fifteen years.

Lump Sum Benefits

- Immediate access to maximum funds

- Fixed interest rate stability

- Simple one-time distribution

- No ongoing management needed

Monthly Payment Benefits

- Guaranteed regular income stream

- Helps with monthly budgeting

- Supplements retirement income

- Predictable cash flow planning

Line of Credit Benefits

- Access funds only when needed

- Unused credit grows over time

- Interest only on withdrawals

- Emergency fund protection

Combination Payment Strategies

Many borrowers combine payout options to maximize benefits from their reverse mortgage. You might take a partial lump sum for immediate needs while establishing a growing line of credit for future expenses. The calculator helps you model different combinations to find the optimal strategy.

Common combinations include a small initial draw with monthly payments, or monthly payments paired with a standby credit line. These mixed approaches provide both regular income and emergency access to funds. Your lender can customize the distribution to match your specific financial objectives.

Benefits of Using a HECM Reverse Mortgage Calculator

HECM calculators deliver valuable insights without requiring you to contact lenders or submit applications. These tools empower you to explore options privately and develop informed questions before speaking with financial advisors. The immediate feedback helps you determine whether a reverse mortgage aligns with your retirement strategy.

Financial Planning and Preparation

Calculator results integrate into broader retirement planning by showing exact equity access amounts. You can compare reverse mortgage proceeds against other financing options like home equity loans or downsizing. This comparison helps determine the most cost-effective way to access needed funds during retirement.

The tool also reveals how different scenarios affect your loan amount. You can adjust home value estimates, test different ages, or explore the impact of paying down existing mortgages before applying. These what-if scenarios provide clarity about timing and preparation steps that maximize your proceeds.

No Obligation Exploration

Using online calculators requires no personal information beyond basic age and property details. You maintain complete privacy while researching your options. No one contacts you, no credit checks occur, and no applications are submitted based solely on calculator usage.

This no-pressure environment encourages thorough exploration of reverse mortgage products. You can return to the calculator multiple times as your situation changes or as you gather more accurate information. The anonymous access removes barriers to education about these complex financial products.

Calculator Advantages

- Instant results without waiting for lender quotes

- Complete privacy during research phase

- Free access to important financial projections

- Ability to test multiple scenarios quickly

- Educational tool for understanding HECM mechanics

- Foundation for informed lender conversations

- Comparison capability across different ages and values

Calculator Limitations

- Estimates only, not guaranteed loan amounts

- Cannot account for all individual circumstances

- Simplified calculations may miss complex factors

- Interest rate assumptions may differ from actual offers

- Does not replace professional financial advice

- Results vary between different calculator tools

Time and Resource Efficiency

Calculators streamline the initial research process by delivering immediate feedback. Instead of scheduling multiple lender meetings to gather quotes, you gain foundational knowledge in minutes. This efficiency proves especially valuable when comparing reverse mortgages against alternative financial strategies.

The time saved through calculator usage allows you to focus conversations with lenders on specific questions and concerns. You arrive prepared with realistic expectations about loan amounts and costs. This preparation leads to more productive discussions and faster decision-making when you’re ready to proceed.

While HECM calculators provide valuable estimates, they have inherent limitations that users must understand. These tools simplify complex calculations that involve dozens of variables and individual circumstances. Recognizing what calculators cannot account for helps you use them appropriately within your research process.

Estimate Accuracy Considerations

Calculator results represent estimates based on standardized formulas and assumptions. Actual loan amounts may vary when lenders perform detailed property appraisals and credit analyses. The calculator cannot account for property condition issues, title problems, or unique circumstances that affect final approval amounts.

Interest rate assumptions in calculators use current market averages or default rates. Your actual rate depends on the specific lender, your credit profile, and market conditions at closing time. Even small interest rate differences can significantly impact your principal limit and available proceeds.

Missing Individual Circumstances

Generic calculators cannot evaluate your complete financial picture or personal situation. They don’t consider your other debts, income sources, or long-term care needs. These factors may influence whether a reverse mortgage represents the best solution for your specific circumstances.

Property-specific issues also fall outside calculator capabilities. Unique home features, location factors, or market conditions in your area affect actual appraisal values. Co-op apartments, manufactured homes, or properties with multiple units require specialized evaluations that standard calculators cannot provide.

Important Calculator Limitations

Remember that calculator results serve as preliminary estimates only. Final loan amounts depend on professional appraisals, FHA lending limits in your area, lender-specific requirements, credit and title review results, current market interest rates at closing, and property condition assessment. Always consult with licensed HECM professionals before making financial decisions based solely on calculator estimates.

Comparison Challenges Between Tools

Different calculators may produce varying results based on their underlying assumptions and formulas. Some tools use conservative estimates while others project more optimistic scenarios. This variance can confuse borrowers trying to understand their realistic borrowing capacity.

Calculator sophistication levels differ significantly across websites. Basic tools provide simple estimates while advanced calculators offer detailed breakdowns of fees, insurance costs, and long-term projections. The quality and accuracy of results depend heavily on the calculator’s design and the data sources it uses.

Understanding HECM Costs and Fees

HECM reverse mortgages involve several costs that reduce the net proceeds you receive. Calculators typically display these fees to show the difference between your principal limit and actual available funds. Understanding each cost component helps you evaluate the true expense of accessing your equity through a reverse mortgage.

Origination Fees and Lender Charges

Lenders charge origination fees for processing your reverse mortgage application and managing the loan setup. FHA regulations cap these fees at $2,500 for homes valued under $200,000, with higher limits for more expensive properties. The calculator deducts this amount from your principal limit to show net proceeds.

Some lenders offer reduced or waived origination fees as competitive incentives. These promotional offers can increase your net proceeds by thousands of dollars. When comparing actual lender quotes, pay close attention to origination fee variations that calculators may not reflect.

Mortgage Insurance Premiums

FHA requires two types of mortgage insurance for HECM loans that protect both borrowers and lenders. An initial mortgage insurance premium of 2% of the home value is due at closing. The calculator factors this substantial cost into your net proceeds calculation.

Ongoing mortgage insurance costs 0.5% annually of the outstanding loan balance. This amount accrues to your loan balance over time rather than requiring monthly payments. While calculators show the initial premium, they may not project long-term insurance accumulation over years or decades.

Third-Party Closing Costs

Standard closing costs apply to reverse mortgages just like traditional mortgages. These include appraisal fees, title insurance, recording fees, and credit checks. Total closing costs typically range from $2,000 to $6,000 depending on property location and value.

The calculator estimates these costs based on average figures for your area. Actual expenses may vary when you receive specific quotes from title companies and other service providers. Some costs like appraisal fees are paid upfront, while most closing costs come from your loan proceeds.

| Cost Category | Typical Amount | Payment Timing | Calculator Treatment |

| Origination Fee | $2,500 – $6,000 | At closing from loan proceeds | Deducted from principal limit |

| Initial MIP | 2% of home value | At closing from loan proceeds | Deducted from principal limit |

| Annual MIP | 0.5% of loan balance | Accrues monthly to balance | May not be shown in simple calculators |

| Appraisal Fee | $450 – $800 | Paid upfront before closing | Included in closing cost estimate |

| Title Insurance | $700 – $1,500 | At closing from loan proceeds | Included in closing cost estimate |

| Recording Fees | $100 – $400 | At closing from loan proceeds | Included in closing cost estimate |

| Counseling Fee | $125 – $200 | Paid before application | Rarely included in calculations |

Ongoing Responsibilities and Costs

Reverse mortgage borrowers must continue paying property taxes, homeowners insurance, and home maintenance costs. These obligations don’t appear in calculator projections but represent critical ongoing expenses. Failure to maintain these payments can trigger loan default and foreclosure.

Some borrowers choose to set aside a portion of loan proceeds for future property tax and insurance payments. This strategy, called a Life Expectancy Set Aside, ensures funds remain available for these mandatory expenses. Calculators typically don’t automatically factor in these voluntary set-asides.

HECM Versus Other Reverse Mortgage Options

The Home Equity Conversion Mortgage represents just one type of reverse mortgage product available to seniors. Understanding how HECM compares to alternatives helps you choose the most appropriate equity access strategy. Each option carries distinct advantages, limitations, and ideal use cases that calculators can help evaluate.

Proprietary Reverse Mortgages

Proprietary reverse mortgages are private loans offered by individual lenders without FHA insurance. These products typically serve borrowers with high-value homes exceeding FHA lending limits. Proprietary loans may provide larger loan amounts for expensive properties but lack the consumer protections of HECM products.

Calculators for proprietary reverse mortgages function similarly to HECM tools but use different lending limits and fee structures. Interest rates on proprietary products may be higher, and fewer payout options might be available. These loans suit homeowners whose property values far exceed the FHA maximum lending limit in their area.

Single-Purpose Reverse Mortgages

Single-purpose reverse mortgages are offered by state and local government agencies or nonprofits for specific uses. These loans fund particular expenses like property taxes or home repairs. They feature the lowest costs among reverse mortgage options but strictly limit how you can use the money.

Standard HECM calculators don’t apply to single-purpose products because lending criteria differ significantly. These specialized loans may not require age 62 eligibility and often have income restrictions. Availability varies by location, and loan amounts are typically much smaller than HECM or proprietary options.

HECM Reverse Mortgage

- FHA-insured with consumer protections

- Nationwide availability through approved lenders

- Multiple payout options available

- Regulated fees and terms

- Non-recourse loan guarantee

- Mandatory counseling required

Best for: Most seniors seeking flexible equity access with maximum protections

Proprietary Reverse Mortgage

- No FHA lending limits

- Higher loan amounts for expensive homes

- Fewer consumer protections

- Limited lender availability

- Potentially higher costs

- Varying qualification requirements

Best for: Owners of high-value homes exceeding FHA limits

Single-Purpose Reverse Mortgage

- Lowest cost option

- Limited to specific approved uses

- Income restrictions may apply

- Not available in all areas

- Smaller loan amounts

- Government or nonprofit funding

Best for: Low-income seniors needing help with property taxes or repairs

Home Equity Loans and Lines of Credit

Traditional home equity loans and HELOCs represent alternatives to reverse mortgages that require monthly mortgage payments. These products may offer lower interest rates and fees but demand income verification and debt-to-income qualification. Borrowers must make regular payments that can strain fixed retirement incomes.

Home equity loan calculators show monthly payment obligations that reverse mortgage calculators deliberately avoid. This fundamental difference highlights the primary advantage of reverse mortgages: accessing equity without adding monthly mortgage payments to your budget. The tradeoff involves higher upfront costs and interest accumulation over time.

HECM Eligibility Requirements

Meeting HECM eligibility criteria is essential before calculator results become relevant to your situation. These requirements protect borrowers and ensure the program serves its intended purpose of helping seniors age in place. Understanding eligibility parameters helps you determine whether to pursue reverse mortgage options further.

Age and Ownership Requirements

All borrowers must be at least 62 years old to qualify for a HECM reverse mortgage. When multiple people own the property, the youngest borrower’s age determines eligibility and loan amount. Married couples where one spouse is under 62 face special considerations that affect their loan structure and protections.

You must own your home outright or have substantial equity with a low remaining mortgage balance. The property must serve as your primary residence where you live for the majority of each year. Second homes, vacation properties, and investment properties don’t qualify for HECM loans regardless of equity levels.

Property Type and Condition Standards

HECM loans are available for single-family homes, FHA-approved condominiums, and manufactured homes meeting specific requirements. Properties must meet FHA minimum property standards for safety and livability. The required appraisal evaluates both value and condition to ensure the home qualifies.

Multi-unit properties with up to four units can qualify if you occupy one unit as your primary residence. Co-op apartments generally don’t qualify for HECM loans, though some proprietary reverse mortgage programs accept them. The property must be in good repair without major safety issues or deferred maintenance.

Qualified Property Types

- Single-family detached homes

- FHA-approved condominiums

- Manufactured homes built after June 1976

- Two-to-four unit properties with owner occupancy

- Townhouses and planned unit developments

Property Condition Requirements

- Meets FHA minimum property standards

- Structurally sound with safe systems

- No significant deferred maintenance

- Adequate heating and cooling systems

- Roof and foundation in good condition

- No environmental hazards present

Financial Assessment and Obligations

Lenders conduct financial assessments to verify your ability to pay property taxes, insurance, and maintenance costs. This evaluation reviews income, credit history, and existing debts. While reverse mortgages don’t require monthly mortgage payments, you must demonstrate capacity to maintain ongoing property expenses.

Serious delinquencies on property taxes or homeowners insurance in the past two years may disqualify you. Lenders may require a Life Expectancy Set Aside that reserves loan proceeds for future tax and insurance payments if your financial assessment raises concerns. This requirement reduces initial proceeds but ensures you can maintain property obligations.

Mandatory Counseling Requirement

All HECM applicants must complete counseling with a HUD-approved agency before proceeding. This requirement ensures you understand reverse mortgage mechanics, alternatives, costs, and obligations. The counseling session typically costs $125 to $200 and can occur in person, by phone, or via video conference.

Counseling covers how reverse mortgages work, their impact on your estate, and implications for heirs. The counselor helps you evaluate whether a reverse mortgage aligns with your financial goals or if alternatives might serve you better. You receive a certificate after counseling that remains valid for 180 days for loan applications.

Impact on Heirs and Estate Planning

Reverse mortgages significantly affect your estate and the inheritance you leave to heirs. Understanding these implications helps you make informed decisions and prepare your family for eventual loan repayment. Calculators show loan amounts but typically don’t project long-term balance growth that affects estate value.

How Loan Balances Grow Over Time

Your reverse mortgage balance increases as interest and mortgage insurance premiums compound monthly. Unlike traditional mortgages where payments reduce the balance, reverse mortgages accumulate interest on the outstanding amount plus any funds withdrawn. This compounding effect can substantially increase the total debt over decades.

Line of credit withdrawals add to your loan balance immediately, while unused credit continues growing. Monthly payment or tenure options draw funds regularly, steadily increasing what you owe. The loan amount can eventually exceed your original home value, though HECM’s non-recourse feature protects borrowers and heirs from owing more than the home is worth.

Non-Recourse Protection

HECM reverse mortgages include non-recourse provisions that protect borrowers and heirs. When the loan becomes due, repayment is limited to the home’s value at that time. If the loan balance exceeds the property value, FHA mortgage insurance covers the difference. Neither you nor your heirs can be held personally liable for any shortfall between the loan balance and home value.

Repayment Options for Heirs

When the last borrower passes away or permanently leaves the home, heirs have several options for handling the reverse mortgage. They can repay the loan balance and keep the property, sell the home and use proceeds to repay the loan, or turn the property over to the lender if the balance exceeds its value.

Heirs typically have six months to decide on repayment, with possible extensions. If they choose to keep the home, they can refinance the reverse mortgage into a traditional mortgage or pay cash for the balance. Selling the property is the most common option, with any remaining equity after loan repayment going to the estate.

Estate Planning Considerations

Families should discuss reverse mortgage plans openly to avoid surprises later. Heirs who expect to inherit the family home need to understand that reverse mortgages reduce or eliminate that inheritance. Properties with minimal remaining equity after loan repayment may not provide the anticipated legacy.

Some seniors use reverse mortgage proceeds to enhance quality of life now rather than preserving home equity for heirs. This philosophical choice prioritizes current needs over future inheritance. Others carefully manage withdrawals to preserve maximum equity for their estate. Calculator projections of different withdrawal strategies help model these scenarios.

Tips for Making Informed Reverse Mortgage Decisions

Choosing whether to pursue a reverse mortgage requires careful consideration of your complete financial picture. Calculator results provide important data points but represent just one element of comprehensive decision-making. These tips help you evaluate reverse mortgages within the context of your overall retirement strategy.

Comparing Multiple Lender Quotes

Calculator estimates should lead to consultations with several HECM lenders for actual quotes. Interest rates, origination fees, and closing costs vary significantly between lenders. Comparing at least three detailed proposals helps you identify the best terms and maximize net proceeds.

Request itemized good faith estimates that break down all costs and project long-term loan balances. Ask about interest rate options, different payout structures, and any promotional offers or fee waivers. The lender offering the lowest origination fee may not provide the best overall value if their interest rates are higher.

Considering Alternative Solutions

Reverse mortgages solve specific financial challenges but aren’t the only option for accessing home equity or funding retirement. Downsizing to a less expensive home can free up equity while reducing maintenance and tax burdens. Traditional home equity products may work better if you can manage monthly payments from other income sources.

Some seniors benefit more from delaying reverse mortgages until later in retirement when needs are greater. Waiting increases your principal limit as you age and may reduce the total years that interest compounds. Consider whether current financial needs justify immediate equity access or if other resources could bridge shorter-term gaps.

When HECM Makes Sense

- You plan to remain in your home long-term

- You need to eliminate monthly mortgage payments

- You have limited other retirement income sources

- You want to establish an emergency credit line

- Healthcare or home modification costs are needed

- You’re comfortable with reduced estate value

When to Consider Alternatives

- You may move in the next few years

- You can manage traditional loan payments

- You have substantial other assets available

- Preserving home equity for heirs is priority

- You might qualify for government assistance

- Downsizing would solve financial issues

Consulting Financial and Legal Advisors

Professional guidance from financial planners and estate attorneys provides valuable perspective on reverse mortgage decisions. These advisors evaluate how reverse mortgages interact with your complete financial plan, tax situation, and estate goals. Their objective analysis helps identify potential issues calculator results don’t reveal.

Ask advisors to review your calculator results and lender quotes before proceeding. They can spot unfavorable terms, suggest alternative strategies, or confirm that a reverse mortgage aligns with your objectives. The cost of professional advice is minimal compared to the major financial commitment a reverse mortgage represents.

Understanding Your Complete Costs

Look beyond initial fees to understand the total cost of your reverse mortgage over time. Project how much interest will accumulate over 10, 15, or 20 years based on different interest rates. Compare these projections against the value of having immediate access to your equity for current needs.

Consider opportunity costs of money tied up in your home versus liquid investments. Calculate whether investment returns on freed equity might offset reverse mortgage costs. Factor in the value of remaining in your home versus potential assisted living expenses if you were to move.

Ready to Explore Your HECM Options?

Whether you want to calculate your potential loan amount, speak with a licensed specialist about your unique situation, or receive detailed information about reverse mortgages, we’re here to help with no obligation.

Choose the option that works best for you. All consultations are free, confidential, and carry no obligation to proceed.

Common Mistakes When Using HECM Calculators

Users frequently make errors when inputting information or interpreting calculator results. These mistakes can lead to unrealistic expectations or poor financial decisions. Recognizing common pitfalls helps you use calculators more effectively and avoid disappointment when receiving actual lender quotes.

Inaccurate Home Value Estimates

Overestimating your property value is the most common calculator mistake that inflates loan amount projections. Many homeowners base estimates on outdated assessments, peak market values, or wishful thinking. Professional appraisals often come in lower than owner estimates, reducing actual loan proceeds below calculator projections.

Use recent comparable sales in your neighborhood for realistic value estimates. Online valuation tools provide starting points but carry significant margins of error. If your calculator results seem too good to be true based on property values, verify your estimate with a real estate professional before getting excited.

Misunderstanding Interest Rate Assumptions

Calculator interest rates significantly impact results, but users often overlook what rates the tool assumes. Some calculators use optimistic rate projections while others apply conservative estimates. Small rate differences of just half a percent can change loan amounts by tens of thousands of dollars.

Always check what interest rate the calculator uses in its assumptions. Compare this rate to current market conditions for HECM loans. Remember that adjustable rates consist of an index plus a margin, and both components affect your actual loan terms. If possible, run calculations with multiple rate scenarios to understand potential variation.

Overlooking Existing Mortgage Balance Impact

Borrowers sometimes focus on gross loan amounts without adequately considering existing mortgage payoff requirements. The calculator may show a principal limit of $200,000, but if you owe $120,000 on your current mortgage, your net proceeds drop to $80,000 or less after fees. This dramatic difference surprises many users.

Always enter accurate remaining mortgage balances into calculators that request this information. Understand that this debt must be paid off before you receive any cash proceeds. Properties with large existing mortgages may not generate enough net proceeds to justify reverse mortgage costs and complexity.

Calculator Accuracy Checklist

Before trusting calculator results, verify these key inputs:

- Home value based on recent comparable sales, not tax assessments

- Exact remaining mortgage balance from your latest statement

- Age of the youngest borrower, not oldest

- Current market interest rates for HECM loans

- Property type correctly selected (single-family, condo, etc.)

- Your actual primary residence, not a second home

Accurate inputs produce reliable estimates that help you make better decisions.

Ignoring Calculator Disclaimers

Most calculators include disclaimers explaining that results are estimates only and actual amounts may vary. Users eager to see positive numbers often skip these important warnings. The disclaimers protect calculator providers but also provide valuable context about result limitations.

Read disclaimers carefully to understand what the calculator can and cannot determine. Note any assumptions about fees, rates, or other factors that could change. These warnings help set realistic expectations and remind you that calculator results begin rather than conclude your research process.

Special Situations and Calculator Scenarios

Certain circumstances require special consideration when using HECM calculators. These unique situations affect eligibility, loan amounts, or the appropriateness of reverse mortgages for your needs. Understanding how calculators handle or fail to address special scenarios prevents misunderstandings during the application process.

Non-Borrowing Spouse Considerations

When one spouse is under age 62, they cannot be a co-borrower on the HECM loan. The older spouse borrows alone, with special protections for the younger non-borrowing spouse. This situation affects loan amounts and creates unique considerations that standard calculators may not address.

The calculator uses only the borrowing spouse’s age, potentially showing higher loan amounts than if both ages were considered. However, lenders may require that non-borrowing spouses be added to the loan as eligible non-borrowing spouses with specific protections. These protections allow them to remain in the home after the borrowing spouse passes, but may reduce initial loan proceeds.

Divorced or Widowed Borrowers

Single borrowers often find reverse mortgages particularly beneficial for managing retirement on one income. Widowed homeowners may need to replace lost spousal income or pension benefits. Calculators work normally for single borrowers without the complexity of multiple ages and ownership interests.

Divorced individuals should ensure their divorce decree clearly establishes sole ownership before proceeding. Any claims by former spouses on property title can complicate or prevent reverse mortgage approval. Clear title is essential, and calculator results assume you have undisputed ownership rights.

Trust-Owned Properties

Properties held in living trusts can qualify for HECM loans if the trust meets specific FHA requirements. The trust must be revocable, and the borrower must be both the borrower and beneficiary. These technical requirements don’t affect calculator results but can impact actual loan approval.

If your home is in a trust, mention this when consulting with lenders even if calculator results look favorable. Some lenders have more experience with trust-owned properties than others. Trust documents will need review during the application process to confirm compliance with FHA guidelines.

Properties Needing Repairs

Homes requiring significant repairs may not qualify until issues are addressed. The FHA appraisal identifies necessary repairs that must be completed before closing. Calculator results don’t account for repair costs that might need to come from loan proceeds, reducing your actual net available funds.

Major repairs like roof replacement or foundation work can consume tens of thousands of dollars from your proceeds. If you know your property needs work, budget these costs when evaluating calculator results. Some borrowers use reverse mortgage proceeds specifically to fund needed repairs while eliminating mortgage payments.

Regulatory Protections and Consumer Safeguards

HECM reverse mortgages include numerous consumer protections mandated by FHA and federal law. These safeguards protect borrowers from predatory practices and ensure informed decision-making. Understanding these protections provides confidence when considering reverse mortgages and helps you recognize reputable lenders.

FHA Insurance and Non-Recourse Features

Every HECM carries FHA insurance that protects both borrowers and lenders. This insurance guarantees you’ll receive loan proceeds even if your lender fails. It also provides the non-recourse protection ensuring you never owe more than your home’s value, regardless of loan balance growth.

The non-recourse feature represents one of the most valuable HECM protections. If your loan balance eventually exceeds your property value, FHA insurance covers the difference when the loan is repaid. Neither you nor your heirs face personal liability for any shortfall. This protection applies even if home values decline significantly during your loan term.

Mandatory Counseling Requirements

Required counseling sessions with HUD-approved agencies ensure you understand reverse mortgages before committing. Counselors must be independent from lenders and receive training on HECM products. They review alternatives, help you understand costs, and ensure you’re making informed decisions.

The counseling session creates a cooling-off period that discourages rushed decisions. You can ask questions without sales pressure and receive objective information. Many borrowers find that counseling either confirms their reverse mortgage decision or reveals better alternatives they hadn’t considered.

Right to Rescind and Cancel

After closing your reverse mortgage, you have three business days to cancel the loan for any reason. This rescission period provides a final opportunity to change your mind without penalty or obligation. All funds advanced to you must be returned, and the lender cancels the mortgage as if it never existed.

Some states provide additional consumer protections beyond federal requirements. These might include extended rescission periods or additional disclosure requirements. Your lender must inform you of all applicable rights and protections at closing time.

Can the lender take my home if I default on property taxes or insurance?

While you cannot be foreclosed for missing reverse mortgage payments (since there aren’t any), you must maintain property taxes, insurance, and basic maintenance. Failing to meet these obligations for extended periods can trigger default provisions. However, lenders must work with you to resolve issues before initiating foreclosure. FHA requires lenders to explore all options including payment plans and assistance programs before taking serious action.

What protections exist for surviving spouses?

Eligible non-borrowing spouses can remain in the home even after the borrowing spouse passes away. They cannot access additional loan proceeds but don’t have to repay the loan immediately. This protection applies to spouses who were married to the borrower at loan origination and closing, and who have lived in the home as their primary residence throughout the loan term.

How does FHA insurance protect me as a borrower?

FHA insurance provides multiple borrower protections: it guarantees you’ll receive all loan proceeds even if your lender fails, ensures you cannot be forced to repay more than 95% of the home’s appraised value, protects your ability to remain in the home if you meet loan obligations, and covers lender losses if the loan balance exceeds property value at repayment.

Are there protections against predatory lending practices?

HECM loans include numerous anti-predatory lending protections: lenders cannot pressure you to purchase other financial products, mandatory counseling must occur before application, all fees and charges are capped and regulated by FHA, lenders cannot require you to purchase annuities or investments, and all loan terms must be clearly disclosed in writing with time to review.

Frequently Asked Questions About HECM Calculators

These common questions address specific concerns and scenarios that borrowers encounter when using HECM calculators. The answers provide practical guidance for interpreting results and understanding how various factors influence your reverse mortgage options.

How accurate are online HECM calculator results?

Online calculators provide reasonable estimates when you input accurate information. Results typically fall within 5-10% of actual lender quotes for borrowers with straightforward situations. However, final loan amounts depend on professional appraisals, exact interest rates at closing time, your specific lender’s fees, and individual circumstances that calculators cannot evaluate. Treat calculator results as helpful starting points rather than guaranteed amounts.

Why do different calculators show different results for the same inputs?

Calculators use varying assumptions about interest rates, closing costs, and fee structures. Some tools apply conservative estimates while others use optimistic projections. Different calculators may use slightly different formulas or principal limit factor tables. The sophistication level varies too, with basic calculators providing simple estimates and advanced tools offering detailed breakdowns. These variations explain why you might see results differing by $10,000 or more between calculators.

Should I use my tax assessment value or estimated market value in the calculator?

Always use current estimated market value rather than tax assessment values. Tax assessments often lag behind market values and may not reflect actual selling prices in your area. Research recent comparable home sales in your neighborhood or consult with local real estate agents for realistic value estimates. Overestimating value leads to disappointment when actual appraisals come in lower, while underestimating means missing potential loan proceeds.

Can I use calculator results when comparing different lenders?

Calculator results help you understand general reverse mortgage mechanics but shouldn’t replace actual lender quotes. Each lender offers different interest rates, margin rates, and origination fees that significantly impact your net proceeds. Request detailed good faith estimates from multiple lenders showing all costs and loan terms. Compare these actual quotes rather than relying solely on generic calculator projections.

How often should I recalculate my potential reverse mortgage amount?

Recalculate annually or whenever significant changes occur in your situation. Home values fluctuate with market conditions, affecting your potential loan amount. Interest rates change monthly, impacting how much you can borrow. Your age increases annually, raising your principal limit. If you’re not ready to proceed immediately, checking updated figures every 6-12 months keeps you informed about your options as conditions change.

Do calculator results account for all the fees I’ll pay?

Most calculators include major fees like origination charges, initial mortgage insurance premiums, and estimated closing costs. However, they may not capture every small fee or cost specific to your situation. Calculators also typically don’t project ongoing annual mortgage insurance costs that accrue to your balance. For complete fee disclosure, request itemized good faith estimates from actual lenders showing every charge you’ll encounter.

What if my calculator result seems too low to be worth pursuing?

Low results might indicate insufficient equity after mortgage payoff, high existing debt, or that you’re on the younger end of eligibility. However, calculator inaccuracies could also be at fault. Verify your inputs are correct and try different calculators for comparison. Consult with a HECM specialist who can evaluate your complete situation and potentially identify ways to improve your loan amount, such as paying down your existing mortgage before applying.

Can I save calculator results to compare with future calculations?

Most online calculators don’t save your results automatically, so take screenshots or write down key figures for future reference. Note the date, interest rate used, and all inputs so you can compare accurately when you recalculate later. Some advanced calculator tools allow you to create accounts that save multiple scenarios. Tracking your results over time helps you identify the optimal moment to proceed based on age increases and market conditions.

Moving Forward With Confidence

HECM reverse mortgage calculators serve as powerful tools for understanding your home equity access options during retirement. These calculators process complex formulas instantly, showing you potential loan amounts based on your age, home value, and current market conditions. The insights they provide form the foundation for informed financial decisions about accessing equity without monthly mortgage payments.

Remember that calculator results represent estimates rather than guaranteed loan amounts. Professional appraisals, lender-specific terms, and your individual circumstances will determine actual proceeds. Use calculator projections to start conversations with family members, financial advisors, and licensed HECM specialists who can provide personalized guidance.

The decision to pursue a reverse mortgage deserves careful consideration of your complete financial picture. Evaluate how reverse mortgages compare to alternatives like downsizing, home equity loans, or other retirement funding strategies. Consider the impact on your estate and discuss plans with heirs to ensure everyone understands the implications.

Take advantage of the no-obligation nature of calculator usage and HUD-required counseling. Gather information, ask questions, and explore your options thoroughly before committing. The time invested in research and consultation pays dividends in confidence and peace of mind about your decision.

Whether you proceed with a reverse mortgage or choose alternative solutions, the knowledge gained through calculator usage and education serves you well. You’ll understand how home equity can support retirement goals and what options exist for accessing this valuable resource when needs arise.

For personalized guidance on your reverse mortgage options and to receive detailed calculations based on your specific situation, call +1 (800) 555-1234 to speak with a HECM specialist. Take the next step toward understanding how your home equity can enhance your retirement security.