Your Complete Guide to Calculating Borrowing Power

Your home represents more than shelter. It holds financial power you can unlock through home equity loans. Understanding how much you can borrow starts with knowing how to calculate your available equity.

A home equity loan calculator simplifies complex math. It shows your borrowing potential based on your home value, existing mortgage balance, and lender requirements. This tool helps you plan major expenses without guesswork.

Whether you’re considering home renovations, debt consolidation, or education costs, accurate calculations make the difference. Let’s explore how these calculators work and what they reveal about your financial options.

What Is a Home Equity Loan Calculator and How Does It Work

A home equity loan calculator is a digital tool that estimates how much money you can borrow against your home. The calculator processes your home value, current mortgage balance, and desired loan terms to show potential loan amounts and monthly payments.

These calculators use your home equity as the foundation. Equity represents the difference between your property value and what you still owe on your mortgage. Most lenders allow you to borrow up to 80-85% of your home value minus your mortgage balance.

The calculation follows a simple formula. First, multiply your home value by the lender’s maximum loan-to-value ratio. Then subtract your current mortgage balance. The result shows your potential borrowing power.

Key Inputs Required for Accurate Calculations

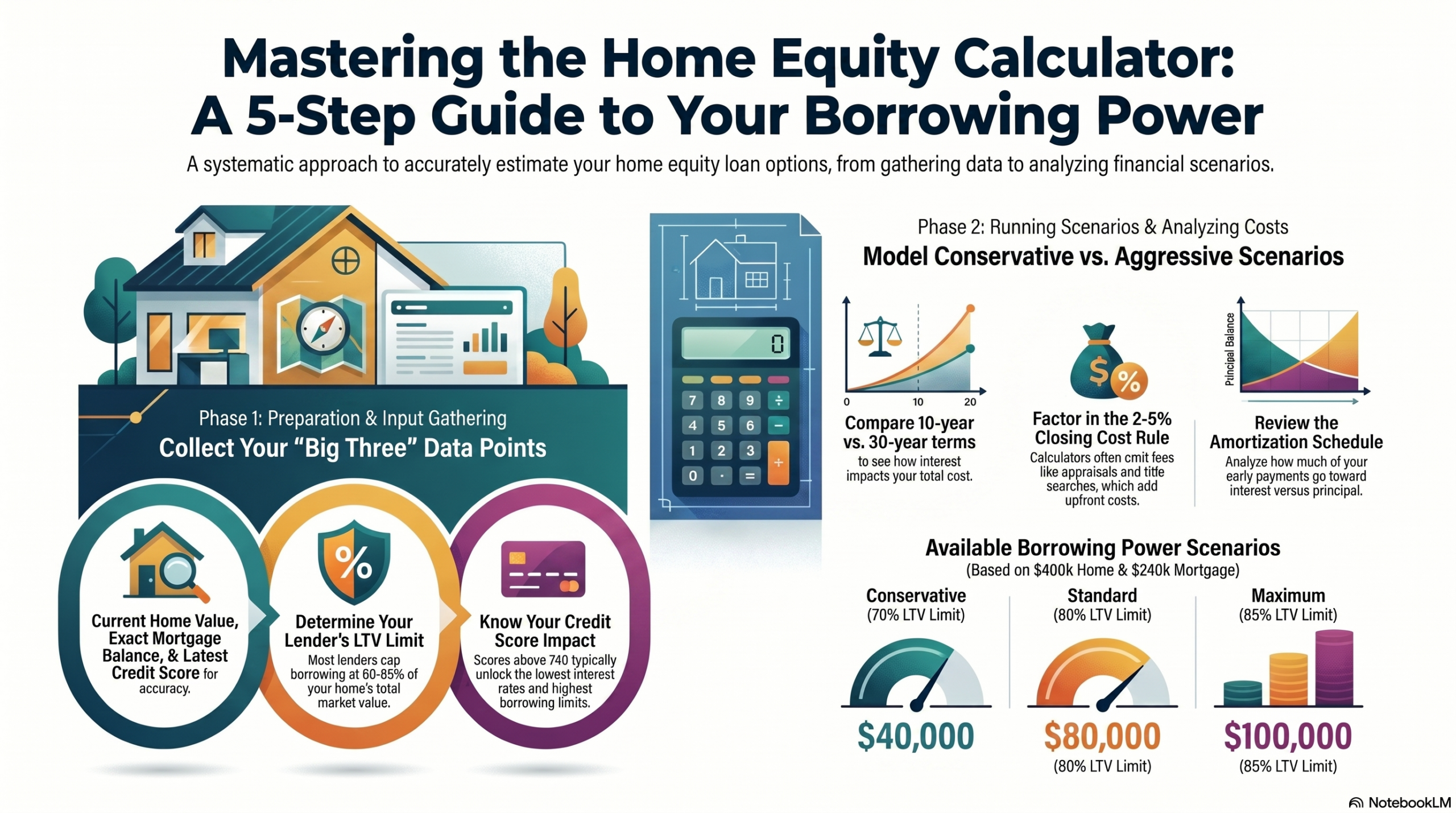

You need specific information to get reliable results from any home equity loan calculator. Start with your current home value, which you can estimate through recent appraisals or comparable sales in your neighborhood.

Home Value Information

Your property’s current market value determines borrowing capacity.

- Recent home appraisal amount

- Comparable property sales data

- Online valuation estimates

- Tax assessment values

Mortgage Details

Outstanding balance affects available equity for borrowing.

- Current mortgage balance

- Original loan amount

- Years remaining on mortgage

- Current interest rate

Loan Preferences

Your desired terms shape monthly payment calculations.

- Preferred loan amount

- Desired repayment term

- Fixed or variable rate

- Estimated interest rate

Financial Qualifications

Lender requirements impact final approval amounts.

- Credit score range

- Debt-to-income ratio

- Employment status

- Monthly income amount

Your credit score plays a vital role in determining interest rates. Higher scores typically secure lower rates, which reduces your overall borrowing costs and monthly payments.

Understanding Calculator Results

Calculator results show more than just a loan amount. You’ll see estimated monthly payments based on different loan terms and interest rates. These projections help you plan your budget.

Most calculators display total interest costs over the loan term. This number reveals the true cost of borrowing and helps you compare different loan options effectively.

The loan-to-value ratio appears in your results. This percentage indicates how much of your home value you’re borrowing. Lower ratios often mean better terms and lower interest rates from lenders.

Ready to See Your Actual Borrowing Power?

Compare personalized rates from multiple lenders in minutes. No obligation and no impact to your credit score.

Critical Factors That Affect Home Equity Loan Calculations

Several elements determine your final loan amount and payment terms. Understanding these factors helps you maximize your borrowing potential while securing favorable rates.

Property Value and Market Conditions

Your home value directly impacts how much equity you can access. Real estate markets fluctuate, affecting your property’s worth over time. Rising home values increase your available equity, while declining markets reduce it.

Lenders typically require professional appraisals to confirm your home value. The appraisal process examines your property’s condition, location, size, and recent comparable sales in your area.

Location matters significantly. Homes in stable or appreciating neighborhoods often qualify for higher loan-to-value ratios. Properties in declining areas may face stricter lending limits.

Loan-to-Value Ratio Requirements

The LTV ratio represents the percentage of your home value that lenders allow you to borrow. Most lenders cap this ratio between 80% and 85%, though some offer up to 90% for qualified borrowers.

A lower LTV ratio typically means better loan terms. Borrowers with LTV ratios under 80% often receive more competitive interest rates and lower closing costs.

Combined Loan-to-Value (CLTV)

When you have multiple loans secured by your home, lenders calculate CLTV. This includes your first mortgage plus any home equity loan or home equity line of credit.

For example, if your home is worth $400,000 with a $240,000 mortgage balance and you want a $40,000 home equity loan, your CLTV would be 70%. This healthy ratio improves your approval chances.

LTV Calculation Example

- Home Value: $400,000

- Maximum LTV: 85%

- Maximum Loan: $340,000

- Current Mortgage: $240,000

- Available Equity: $100,000

- Actual Borrowing Power: $100,000

Interest Rates and Their Impact

Interest rates directly affect your monthly payments and total borrowing costs. These rates vary based on market conditions, your credit score, and the lender you choose.

Fixed-rate home equity loans maintain the same interest rate throughout the loan term. This stability makes budgeting easier since your monthly payment never changes.

Your credit score heavily influences the rate you receive. Borrowers with scores above 740 typically qualify for the lowest rates. Scores below 670 may face significantly higher costs.

Loan Terms and Repayment Periods

Home equity loans typically offer repayment terms between 5 and 30 years. Shorter terms mean higher monthly payments but less total interest. Longer terms reduce monthly costs but increase overall interest paid.

A 10-year term on a $50,000 loan at 7% interest costs about $580 monthly. Extending to 20 years drops payments to roughly $388 monthly but adds thousands in interest charges.

Important: While longer terms seem attractive due to lower monthly payments, you’ll pay significantly more in total interest over the life of the loan. Calculate both options to make an informed decision.

How to Use a Home Equity Loan Calculator for Best Results

Getting accurate calculator results requires preparation and understanding. Follow these steps to maximize the tool’s effectiveness and gain realistic expectations.

Gathering Accurate Financial Information

Start by collecting current documentation. Your most recent mortgage statement shows your exact balance. This precision matters because even small errors in your mortgage balance can significantly affect calculated results.

Check your property’s current value through multiple sources. Online estimators provide quick approximations, but professional appraisals offer definitive values. Recent sales of similar homes in your neighborhood give realistic benchmarks.

Know your credit score before using calculators. Many tools adjust interest rate estimates based on credit ranges. You can access free credit reports from major bureaus to confirm your score.

Running Multiple Scenarios

Test different loan amounts and terms to compare options. Starting with various scenarios helps you understand how changes affect your monthly budget and total costs.

Conservative Scenario

- Lower loan amount (60% LTV)

- Shorter repayment term (10 years)

- Higher monthly payment

- Less total interest paid

- Faster equity rebuilding

Moderate Scenario

- Medium loan amount (75% LTV)

- Standard term (15 years)

- Balanced monthly payment

- Moderate total interest

- Steady equity rebuilding

Aggressive Scenario

- Maximum loan amount (85% LTV)

- Longer term (20-30 years)

- Lower monthly payment

- Higher total interest paid

- Slower equity rebuilding

Compare how interest rate changes affect payments. Even a 0.5% rate difference can save thousands over a loan term. This comparison helps you understand the value of improving your credit score before applying.

Interpreting Payment Schedules

Advanced calculators show amortization schedules. These breakdowns reveal how much of each payment goes toward principal versus interest. Early payments contain more interest, while later payments reduce principal faster.

Understanding this schedule helps you plan extra payments strategically. Additional principal payments early in the loan term reduce total interest costs more effectively than later payments.

Accounting for Additional Costs

Calculator results typically show only principal and interest. Remember to factor in closing costs, which usually range from 2% to 5% of the loan amount.

- Appraisal fees ($300-$500)

- Title search and insurance ($700-$1,000)

- Origination fees (0.5%-1% of loan)

- Recording fees ($50-$250)

- Attorney fees if required ($500-$1,500)

Some lenders offer no-closing-cost options. These loans typically charge higher interest rates to offset upfront expenses. Calculate whether paying costs upfront or through higher rates makes better financial sense for your situation.

Compare Personalized Rate Quotes

See what multiple lenders offer based on your specific situation. Get real rates, not estimates.

Home Equity Loan vs HELOC: Calculator Differences

Home equity loans and home equity lines of credit serve different financial needs. Understanding these differences helps you choose the right product and use appropriate calculators.

Structural Differences

A home equity loan provides a lump sum upfront. You receive the full amount at closing and begin repaying immediately with fixed monthly payments. This structure works well for one-time expenses like home renovations or debt consolidation.

A HELOC functions like a credit card secured by your home. You access a credit line during a draw period, typically 5-10 years. You only pay interest on what you borrow, making it flexible for ongoing expenses.

How Calculators Differ

Home equity loan calculators focus on fixed amounts and terms. You input a specific loan amount, interest rate, and repayment period. The results show consistent monthly payments throughout the loan term.

HELOC calculators account for draw and repayment periods. During the draw period, you might pay only interest. The repayment period then requires principal and interest payments, often resulting in higher monthly costs.

Home Equity Loan Benefits

- Fixed interest rates provide payment stability

- Predictable monthly budgeting

- Lump sum for large one-time expenses

- Simple repayment structure

- Protection from rising rates

HELOC Advantages

- Flexible access to funds as needed

- Pay interest only on amounts used

- Revolving credit during draw period

- Potential for lower initial payments

- Useful for ongoing project costs

Interest Rate Considerations

Home equity loans typically carry fixed interest rates. Your rate remains constant, making long-term planning straightforward. Current fixed rates generally range from 6% to 10%, depending on credit and market conditions.

HELOCs usually feature variable interest rates tied to the prime rate. When the Federal Reserve adjusts rates, your HELOC rate changes accordingly. This variability creates uncertainty in long-term budgeting.

Some lenders offer fixed-rate HELOC options or conversion features. These hybrid products let you lock in rates on all or part of your balance, combining flexibility with stability.

Which Calculator Should You Use

Choose a home equity loan calculator when you need a specific amount for a defined purpose. The fixed structure suits major one-time expenses like home additions, medical bills, or debt consolidation.

Select a HELOC calculator for ongoing or uncertain expenses. Home renovations spanning months or years benefit from this flexibility. You can also use HELOCs as emergency funds, accessing money only when needed.

Benefits and Risks of Using Home Equity Loans

Home equity loans offer powerful financial advantages but come with serious responsibilities. Understanding both sides helps you make informed borrowing decisions.

Primary Benefits

Home equity loans typically offer lower interest rates than credit cards or personal loans. Because your home secures the debt, lenders view these loans as less risky and pass savings to you through reduced rates.

The interest you pay may qualify for tax deductions if you use funds for home improvements. The Tax Cuts and Jobs Act allows deductions on interest for loans used to buy, build, or substantially improve your home.

- Access large amounts of money at favorable rates

- Fixed monthly payments simplify budgeting

- Potential tax deductions on interest payments

- Longer repayment terms than personal loans

- No restrictions on fund usage

- Consolidate high-interest debt effectively

You can use home equity loan funds for virtually any purpose. Common uses include home renovations that increase property value, education expenses, medical bills, or consolidating multiple high-interest debts into one lower payment.

Significant Risks to Consider

Your home serves as collateral for these loans. Failing to make payments can result in foreclosure, meaning you could lose your home. This risk makes home equity loans fundamentally different from unsecured debt.

Critical Warning: Defaulting on a home equity loan puts your home at risk of foreclosure. Never borrow more than you can comfortably repay, and maintain an emergency fund to cover payments during financial hardship.

Borrowing reduces your home equity. If property values decline, you might owe more than your home is worth. This situation, called being “underwater,” creates problems if you need to sell or refinance.

Closing costs add to your borrowing expenses. These fees typically range from 2% to 5% of the loan amount. On a $50,000 loan, you might pay $1,000 to $2,500 in upfront costs before receiving any money.

When Home Equity Loans Make Sense

Consider a home equity loan when you have stable income and strong credit. These factors help you secure better rates and manage payments comfortably.

Good Reasons to Borrow

- Home improvements that increase property value

- Consolidating high-interest debt (over 10% rates)

- Major medical expenses not covered by insurance

- Education costs with expected income return

- Emergency home repairs (roof, foundation, HVAC)

Poor Reasons to Borrow

- Luxury vacations or discretionary purchases

- Daily living expenses or regular bills

- Risky investments or speculative ventures

- Lifestyle expenses beyond your income

- Non-essential items that don’t add value

Evaluate your debt-to-income ratio before borrowing. Lenders typically prefer ratios below 43%. Adding a home equity loan payment shouldn’t push you above this threshold or strain your monthly budget.

Protecting Yourself When Borrowing

Maintain at least 20% equity in your home after borrowing. This cushion protects you if property values decline and provides flexibility for future financial needs.

Shop multiple lenders to compare rates and terms. Rate differences of even 0.25% can save thousands over a loan term. Request quotes from banks, credit unions, and online lenders.

Make an Informed Decision

Download our free home equity loan decision checklist. This comprehensive guide helps you evaluate whether borrowing against your home aligns with your financial goals.

Qualifying for a Home Equity Loan: What Lenders Evaluate

Lenders examine multiple factors before approving home equity loans. Understanding these requirements helps you prepare applications and improve approval chances.

Credit Score Requirements

Most lenders require minimum credit scores between 620 and 680 for home equity loans. Higher scores unlock better interest rates and more favorable terms.

Borrowers with scores above 740 receive the most competitive rates. Those between 680 and 739 qualify but pay moderately higher rates. Scores below 680 face significantly higher costs or potential denial.

Review your credit reports before applying. Dispute any errors that could lower your score. Even small improvements in your credit score can reduce your interest rate and save thousands in total costs.

Debt-to-Income Ratio Standards

Lenders calculate your DTI by dividing monthly debt payments by gross monthly income. This ratio indicates your ability to manage additional debt responsibly.

Most lenders prefer DTI ratios below 43%, though some accept up to 50% for strong borrowers. A lower ratio demonstrates better financial management and increases approval likelihood.

DTI Calculation Example: If your monthly income is $6,000 and you have $1,800 in debt payments (including the proposed home equity loan), your DTI is 30% ($1,800 ÷ $6,000). This healthy ratio should meet most lender requirements.

Income and Employment Verification

Lenders require proof of stable income to ensure repayment ability. You’ll need recent pay stubs, W-2 forms, or tax returns depending on your employment type.

Self-employed borrowers face additional scrutiny. Lenders typically request two years of tax returns and profit-and-loss statements. Consistent income history strengthens your application significantly.

Employment stability matters. Lenders prefer borrowers with steady job history, typically two years or more with the same employer or in the same field.

Equity and Property Requirements

You need sufficient equity to qualify. Most lenders require you to maintain at least 15-20% equity after the loan. This means borrowing up to 80-85% of your home value including your existing mortgage.

Property condition affects approval. Lenders may deny loans on homes needing major repairs. Well-maintained properties in stable neighborhoods receive more favorable consideration.

Application Process Steps

- Pre-qualification: Submit basic financial information for initial assessment

- Formal application: Complete detailed application with supporting documents

- Home appraisal: Lender orders professional property valuation

- Underwriting: Lender reviews all documentation and verifies information

- Approval decision: Lender approves, denies, or requests additional information

- Closing: Sign final documents and receive funds

The process typically takes 30-45 days from application to closing. Some lenders offer expedited timelines for qualified borrowers with complete documentation.

Real-World Home Equity Loan Calculator Examples

Practical examples demonstrate how different scenarios affect loan amounts and monthly payments. These cases illustrate calculator functionality and help you understand potential outcomes.

Example 1: Home Improvement Project

Sarah owns a home valued at $350,000 with a remaining mortgage balance of $180,000. She wants to renovate her kitchen and estimates costs at $40,000.

| Calculation Component | Amount | Details |

| Home Value | $350,000 | Recent appraisal |

| Mortgage Balance | $180,000 | Current amount owed |

| Available Equity | $170,000 | Value minus balance |

| Maximum Loan (85% LTV) | $117,500 | ($350,000 × 85%) – $180,000 |

| Desired Loan Amount | $40,000 | Kitchen renovation cost |

| Loan Term | 10 years | 120 monthly payments |

| Interest Rate | 7.5% | Based on 740 credit score |

| Monthly Payment | $475 | Principal and interest |

| Total Interest Paid | $17,000 | Over loan lifetime |

Sarah qualifies easily with 63% LTV after the loan. Her monthly payment fits comfortably in her budget, and the kitchen renovation should increase her home value by more than the loan cost.

Example 2: Debt Consolidation Strategy

Michael has $25,000 in credit card debt at an average 18% interest rate. His home is worth $280,000 with a $150,000 mortgage balance.

Using a home equity loan calculator, Michael discovers he can borrow $25,000 at 7% over 5 years. His monthly payment would be $495, compared to his current $750 in minimum credit card payments.

Before Home Equity Loan

- Credit card debt: $25,000

- Average interest rate: 18%

- Monthly payment: $750

- Time to pay off: 4.5 years

- Total interest: $15,500

After Home Equity Loan

- Home equity loan: $25,000

- Fixed interest rate: 7%

- Monthly payment: $495

- Loan term: 5 years

- Total interest: $4,700

Michael saves $255 monthly and over $10,000 in total interest. However, he must avoid accumulating new credit card debt or he’ll worsen his financial situation.

Example 3: Education Funding

Jennifer needs $30,000 for her daughter’s college expenses. Her home is valued at $425,000 with a $220,000 mortgage balance and excellent credit.

The calculator shows she can borrow $30,000 at 6.75% for 15 years with monthly payments of $266. She compares this to parent PLUS loans at 8.05% and finds the home equity loan saves money.

Her LTV after the loan is 59%, leaving substantial equity for emergencies. The longer 15-year term keeps monthly costs manageable while her daughter completes school and starts her career.

Example 4: Emergency Home Repairs

David faces unexpected foundation repairs costing $35,000. His home is worth $300,000 with a $200,000 mortgage and a credit score of 680.

The calculator reveals his maximum borrowing capacity is $55,000 at 85% LTV. However, his moderate credit score means an 8.5% interest rate instead of the 7% rate excellent credit borrowers receive.

For a $35,000 loan at 8.5% over 10 years, his monthly payment would be $437. This illustrates how credit scores directly impact borrowing costs—improving his score by 60 points could save him approximately $25 monthly.

See What You Qualify For

Get personalized loan scenarios based on your actual financial situation. Compare multiple lenders and find your best option.

Expert Tips for Maximizing Home Equity Loan Benefits

Strategic planning helps you secure better loan terms and use borrowed funds wisely. These expert recommendations optimize your home equity borrowing experience.

Timing Your Application

Market conditions affect interest rates significantly. Monitor rate trends and apply when rates decline. Even small rate differences compound to substantial savings over loan terms.

Apply when your credit score is highest. Recent late payments or new credit inquiries temporarily lower scores. Wait 3-6 months after negative events before applying for better rates.

Consider seasonal factors. Lenders often compete more aggressively during slower periods like late fall and winter. This competition can result in better rates or reduced closing costs.

Improving Your Qualification Profile

Pay down existing debts before applying. Reducing your debt-to-income ratio increases approval chances and may qualify you for lower rates. Focus on high-interest debts first for maximum impact.

- Check credit reports for errors and dispute inaccuracies

- Pay all bills on time for at least six months before applying

- Reduce credit card balances below 30% of limits

- Avoid opening new credit accounts before application

- Document all income sources comprehensively

- Gather financial records early to expedite processing

Consider increasing your income documentation. Side income, bonuses, or investment returns can strengthen your application. Lenders value diverse, stable income sources.

Shopping for the Best Lender

Compare at least three to five lenders. Rates and fees vary significantly between institutions. Credit unions often offer competitive rates for members, while online lenders may provide faster processing.

Request loan estimates in writing. This standardized document shows all costs and terms clearly. Compare annual percentage rates rather than just interest rates to account for fees.

Negotiate fees and rates. Lenders often have flexibility, especially if you have strong credit and substantial equity. Mention competitive offers to encourage better terms.

Using Borrowed Funds Wisely

Prioritize investments that increase home value or reduce higher-cost debt. These uses provide tangible returns that justify borrowing against your home.

Smart Fund Uses

- Kitchen or bathroom renovations

- Energy-efficient upgrades

- Necessary home repairs

- High-interest debt consolidation

- Education with career benefits

Risky Fund Uses

- Luxury purchases or vacations

- Daily living expenses

- Speculative investments

- Lifestyle inflation

- Non-essential upgrades

Create a detailed budget for borrowed funds. Track every dollar to ensure money serves intended purposes. This discipline prevents waste and helps you stay financially focused.

Managing Repayment Effectively

Set up automatic payments to avoid missed due dates. Late payments damage credit scores and may trigger penalty fees or rate increases on variable products.

Make extra principal payments when possible. Even small additional amounts reduce total interest costs significantly. Specify that extra payments apply to principal, not future interest.

Pro Tip: Making one extra monthly payment per year on a 15-year loan can reduce your repayment period by nearly two years and save thousands in interest charges.

Monitor your home value periodically. Increasing property values strengthen your financial position and may enable refinancing to better terms later. Declining values warrant financial caution.

Avoiding Common Mistakes

Never borrow the maximum available amount unless absolutely necessary. Maintain equity cushion for emergencies and market fluctuations. Financial advisors recommend keeping at least 20% equity.

Don’t ignore total cost calculations. Focus on more than monthly payments. A lower payment with longer term often costs significantly more in total interest over the loan life.

Resist accumulating new debt after consolidation. Many borrowers who consolidate credit cards with home equity loans rack up new credit card balances, compounding their financial problems dangerously.

Alternative Financing Options to Home Equity Loans

Home equity loans aren’t your only option for accessing funds. Understanding alternatives helps you choose the best financing method for your specific situation.

Cash-Out Refinance

A cash-out refinance replaces your existing mortgage with a larger loan. You receive the difference in cash while consolidating debt into one payment at potentially lower rates.

This option makes sense when mortgage rates are lower than your current rate. You refinance to better terms while accessing equity. However, closing costs typically run higher than home equity loans.

Consider cash-out refinancing if you want just one mortgage payment instead of two. The simplified structure may offset slightly higher overall costs for some borrowers.

Personal Loans

Personal loans offer unsecured borrowing without using your home as collateral. This eliminates foreclosure risk but results in higher interest rates and shorter repayment terms.

These loans work well for smaller amounts under $25,000. Processing is faster than home equity loans, often funding within days. No appraisal or home-related fees keep upfront costs minimal.

Personal Loan Advantages

- No home collateral risk

- Faster approval and funding

- No appraisal required

- Lower closing costs

- Flexible loan amounts

Personal Loan Disadvantages

- Higher interest rates (8%-15%+)

- Shorter repayment terms

- Lower maximum amounts

- No tax deductibility

- Higher monthly payments

Credit Cards and Balance Transfers

For short-term needs under $10,000, promotional credit cards or balance transfers might work. Some cards offer 0% APR for 12-21 months, providing interest-free borrowing if you repay quickly.

This strategy requires discipline. Unpaid balances after promotional periods face rates often exceeding 20%. Use only if you can repay before promotional rates expire.

Retirement Account Loans

Some 401(k) plans allow borrowing against your balance. You repay yourself with interest, avoiding lender approval processes. However, this option carries significant risks.

Borrowed amounts don’t grow with market returns. If you leave your job, the full balance typically becomes due immediately. Failure to repay creates taxable distributions plus potential penalties.

Retirement Warning: Borrowing from retirement accounts should be a last resort. The opportunity cost of lost investment growth and potential tax consequences often outweigh the convenience of easy access to funds.

Government Programs

FHA Title I loans finance home improvements up to $25,000 without home equity requirements. These loans help borrowers with limited equity make necessary repairs or upgrades.

Energy-efficient upgrade programs offer special financing through utility companies and government initiatives. These programs sometimes provide below-market rates for qualifying improvements like solar panels or HVAC systems.

Making Informed Home Equity Loan Decisions

Home equity loan calculators provide valuable insights into your borrowing potential. These tools simplify complex calculations and help you understand the financial implications of accessing your home equity.

Understanding how calculators work empowers better financial planning. You can model different scenarios, compare loan options, and determine what fits your budget before speaking with lenders.

Remember that calculator results provide estimates, not guarantees. Actual loan terms depend on lender underwriting, your complete financial profile, and current market conditions. Use calculators as planning tools, then verify details with multiple lenders.

Home equity represents significant financial power. Whether you need funds for home improvements, debt consolidation, education, or emergencies, proper calculation ensures you borrow responsibly without overextending your finances.

Take time to evaluate alternatives and understand the risks. Your home serves as collateral, making responsible borrowing essential. Maintain adequate equity cushion and only borrow amounts you can comfortably repay.

The right home equity loan can help you achieve important financial goals. Armed with calculator insights and comprehensive knowledge, you’re prepared to make decisions that support your long-term financial health and home ownership success.

Take Your Next Step

Whether you’re ready to compare lenders, need personalized advice, or want to download our comprehensive home equity guide, we’re here to help you make the best decision for your situation.